Let’s review the current conditions and then look to history for U.S. stock performance following the beginning of a new rate-cut cycle.

The Fed’s Mission

As you may know, the Fed has a dual mandate of providing price stability and supporting maximum employment across the U.S. economy. Its primary tool for doing so is the fed funds rate, which sets the floor on the cost of borrowing money and, in turn, influences whether businesses and consumers are more likely to spend or save.

Low interest rates tend to promote more borrowing and business spending. High rates encourage saving since bank accounts and fixed-income securities tend to pay higher interest.

Trends that typically lead to interest rate cuts are high unemployment and low inflation. On the flipside, higher inflation and a healthy job market could prompt the Fed to raise rates to cool the economy and prevent excessive price increases for goods and services.

Current Conditions Influencing the Fed

While we’ve made tremendous progress lowering inflation since its post-pandemic peak of 9.1% in 2022, that progress has slowed in recent years. Still, the annual rate of inflation has held above the Fed’s 2.0% target.

Data this month showed the July consumer price index (CPI) rose 2.7% year over year, with core inflation (which excludes the volatile food and energy segments) running at 3.1%. Meanwhile, the producer price index (PPI), which is a gauge of the costs borne by businesses, also rose in July. In combination, the CPI and PPI numbers seem to be showing President Trump’s tariffs are beginning to drive prices higher in certain segments of the economy. We expect higher tariffs will be an ongoing potential source of inflationary pressure.

On the other side of the ledger—the job market—the July employment report was one of the most disappointing in recent memory. Just 73,000 payrolls were created last month, and prior months were revised lower by a combined 258,000 jobs. While the unemployment rate ticked up to just 4.2% (still a healthy number), July marked the weakest three-month average job gain since 2020.

Following that report, Trump fired the head of the Bureau of Labor Statistics (BLS), claiming political affiliations influenced the numbers. The move raises questions about the future reliability of BLS reporting; the BLS calculates both the unemployment rate and the consumer price index each month, and market participants rely on the agency’s reports to be a nonpartisan source of truth.

This uncertainty about both inflation and the labor market means the Fed’s policymakers have a tough job ahead of them to balance that dual mandate, which is impacted by both these economic measures.

However, with inflation still within sight of the Fed’s 2% target, and the labor market showing some slippage, markets are now pricing in about an 85% probability of a September rate cut.

If the Fed cuts rates, what happens next? In theory, a rate cut stimulates the economy and markets will cheer the news. Unfortunately, it’s not so cut and dried.

Stock Market Performance Following Rate Cuts

History shows the market’s performance after a rate cut depends heavily on why the Fed is cutting rates.

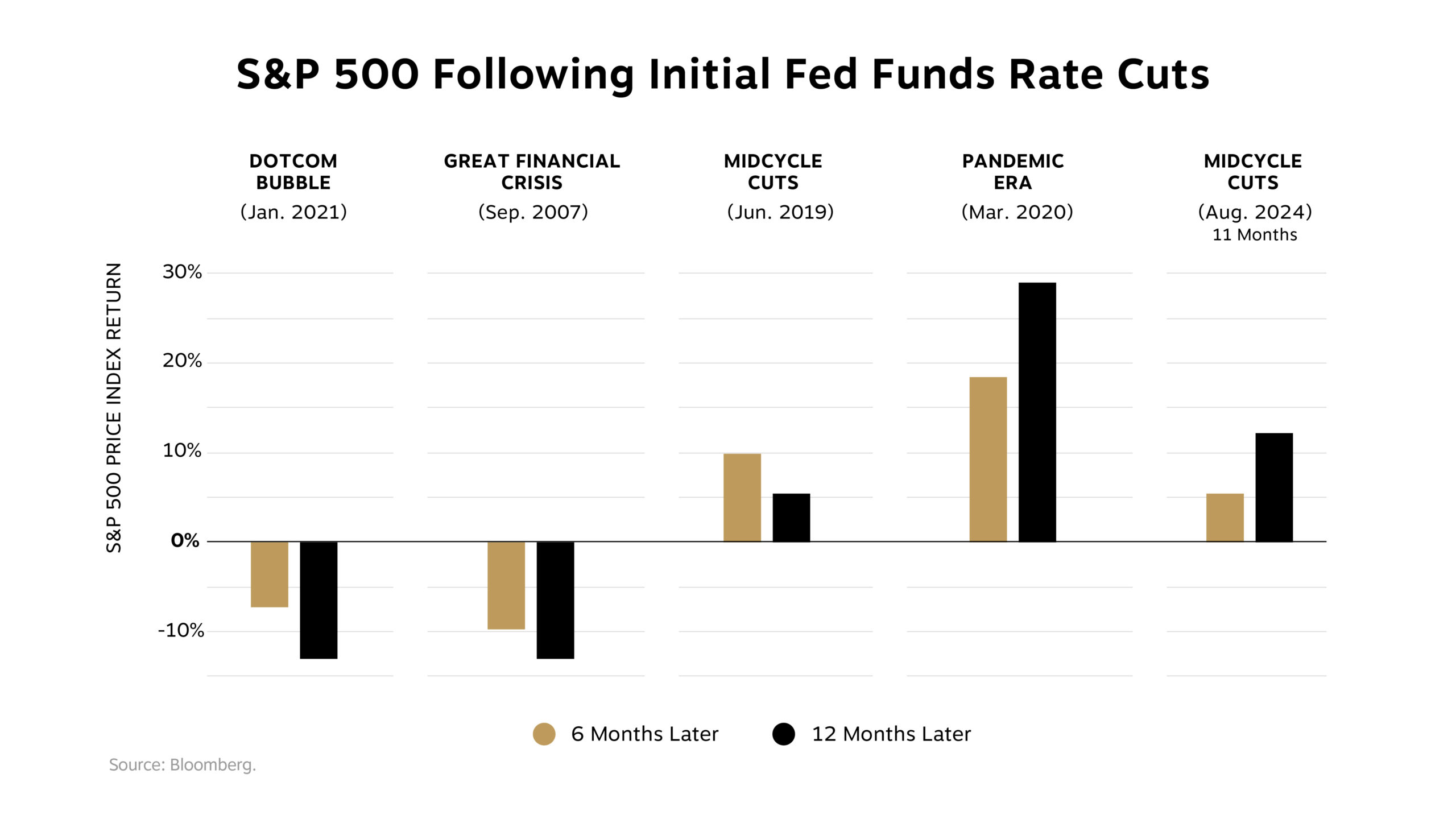

The chart below shows how stocks performed six and 12 months after the Fed made its first rate cut in a new cycle. As you can see, when cuts come as midcycle adjustments with growth still intact, like in 2019 and 2024, forward returns can be positive.

But when cuts are reactive to an oncoming slowdown, results are often negative over the short term. This is what happened after the dotcom bubble burst in the early 2000s and as the subprime mortgage crisis destabilized the financial industry beginning in 2007. (The pandemic era is in its own category—the global economic and market whiplash was so severe and sudden that it’s hard to conclude much from the data except that staying invested through short-term volatility is typically to investors’ benefit.)

Our takeaway is that the economic backdrop should be watched as closely as the policy shift itself. Markets often have knee-jerk reactions to Fed policymaking, but the relationship between stock market returns and central bank activity is complex.

When Will the Fed Decide?

The committee doesn’t officially meet until September 16 and 17, but we expect the action to pick up this month, as the Fed convenes at Jackson Hole for its annual summit. This is often a venue for the Fed chair to announce material changes to its policy stance, and we expect that will be the case again this time around. (Read CEO and Chief Economist Michelle Knight’s takeaways from the Jackson Hole symposium.)

Chair Powell needs to balance evidence of a softer job market with inflation still above target, and he’ll have to address the questions raised by trade policy as well. All this while looking over his shoulder for an impending announcement of his replacement by the president, who has publicly called for rate cuts and questioned the central bank’s policy decisions. Powell, who was appointed by Trump in 2017, is due to run the Fed until May 2026.

For the time being, the focus remains squarely on whether the Fed signals a September cut, but the turmoil at the Fed will surely be a storyline to watch in the months ahead. We are closely monitoring that situation along with economic and market data, and we’re ready to adjust your portfolios to keep them aligned with your goals as circumstances merit.

Our Latest Videos

Chief Investment Officer Joseph “JP” Powers sets the stage for the Federal Reserve’s Jackson Hole summit and its September policy meeting. Click here to watch now!

Partner and Wealth Advisor Jeff Menning, CFP®, reviews impactful provisions from the One Big Beautiful Bill Act and what they mean for your taxes this year and beyond. Watch here.