Newsletter

VOLUME 11 | November 2024

FInancial and tax planning

The ‘Super Catch-up’ and Other Changes Coming in 2025

What do fall foliage, holiday music and the IRS have in common? They all show up as year-end draws near. While the first two items on that list may be more of a presence in your daily life, the annual inflation adjustments to tax brackets and retirement savings contribution limits can make a big difference in your financial and tax planning.

On cue, the IRS recently published 2025 tax bracket information and savings limits for tax-advantaged accounts. In addition, several provisions from the 2022 Secure Act 2.0 will kick in next year, creating more opportunities for retirement savers. This includes the chance for those aged 60 to 63 to supersize their 401(k) catch-up contributions. Let’s review what’s changing.

IRS Inflation Adjustments

This list is not exhaustive, but it covers what we feel is likely most applicable to you in tax year 2025. Note that this is a list of changes at the federal level—your state of residence may impose additional restrictions and limits.

Standard deduction. The standard deduction for married couples filing jointly increased by $800 to $30,000. For singles and taxpayers who are married and filing separately, the deduction is $15,000. For heads of household, the deduction is $22,500.

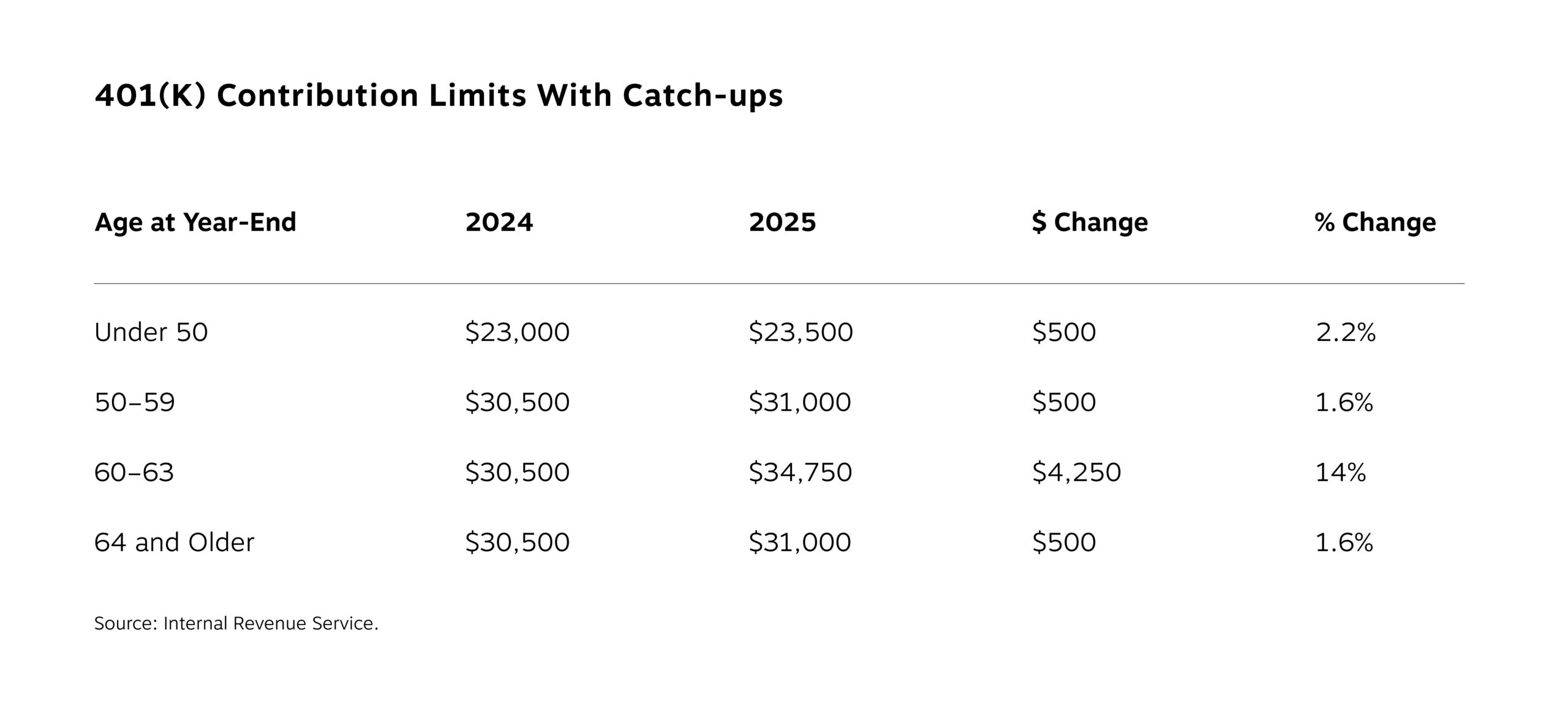

401(k) contribution limits. For 401(k)s, individuals can contribute up to $23,500, up from $23,000 in 2024. If you are age 50 or older, you can invest an additional $7,500, up to $31,000. Next year, investors who turn 60, 61, 62 or 63 during 2025 can sock away an extra $3,750, allowing up to $34,750 in contributions. (See table below for a breakdown.)

IRA contribution limits. Individual retirement account limits are unchanged for 2025; investors can save up to $7,000 and those 50-plus can make $1,000 in catch-up contributions.

Roth IRA phaseout. For Roth IRA contributions, the phaseout for married couples filing jointly is between $236,000 and $246,000, and for single filers it is between $150,000 and $165,000. This does not apply to Roth 401(k) contributors. If your adjusted gross income is over the high end of those ranges, you cannot contribute to a Roth IRA.

Capital gains tax brackets. Income thresholds for long-term capital gains tax rates on assets held longer than 12 months are increasing next year. Notably, single filers earning up to $48,350 in taxable income and married couples filing jointly earning up to $96,700 will pay $0 on realized long-term capital gains. For those taxpayers, this opens the door to selling and repurchasing appreciated assets to reset the cost basis—there is no wash-sale rule on capital gains.

Health care accounts. Employees may get a deduction of $3,300 for their flexible spending accounts (FSAs); for health savings accounts (HSAs), single filers can contribute $4,300 and families can contribute $8,550. After age 55, individuals can contribute an additional $1,000.

Social Security. The cost-of-living adjustment for Social Security for 2025 increases monthly payments by 2.5%.

Estate taxes. The exclusion amount for estates increases to $13,990,000 and the annual exclusion for gifts is rising to $19,000. This higher estate exclusion amount is due to expire at the end of 2025 under current legislation, though the Trump administration may extend the Tax Cuts and Jobs Act passed during its first term.

Retirement Savings Get a Boost From Secure Act 2.0

Two provisions from this landmark legislation go into effect in 2025:

- Supersize me. As noted, savers who reach the ages of 60 to 63 in 2025 can make supersized catch-up contributions to their 401(k) savings accounts. The table below shows the limits by age and the changes from 2024.

- Automatic retirement savings enrollment. In a shift designed to boost participation rates in employer-sponsored retirement plans, companies will automatically enroll eligible employees in their plan if it was established after Secure 2.0 became law on Dec. 29, 2022. Your employer is required to notify you if they are auto-enrolling you and give you the ability to opt out. Employers can specify a contribution amount for you (between 3% and 10% of your salary) unless you make the election yourself.

Catching Up in 2026 May Be More Costly for High Earners

All of the changes above are for 2025, but there’s one Secure 2.0 provision coming down the pike for 2026 that we should begin planning for sooner rather than later. Starting then, catch-up contributions to 401(k) plans will not be tax deductible for people making $145,000-plus a year. Instead, they will be treated like a Roth contribution. This means catch-ups will be made after tax and earnings from them can be withdrawn tax-free in retirement.

Your advisor can help with your tax planning if you will be impacted by this new rule for 2026 or the other adjustments for 2025 we shared above. In the meantime, we hope you’re enjoying the start of the holiday season and all it includes.

The Latest Human Side of Wealth Videos

Chief Investment Officer JP Powers sums up market themes following Donald Trump’s election to a second term as president in Post-Election Update: What’s Next? Watch now!

For more on taxes, watch Smart Year-End Tax Planning, featuring Managing Director, Wealth Management Steve Reder and Director of Financial Planning Andrew Busa.

Charitable Giving

Season of Giving: Why To Consider Donor-Advised Funds

Donor-advised funds (DAFs) are a popular vehicle for charitable giving. As we approach the end of the year—a time when many are considering their charitable contributions—it’s important to understand the advantages of DAFs, especially given the current stock market conditions and the potential tax benefits these funds can offer.

Understanding DAFs

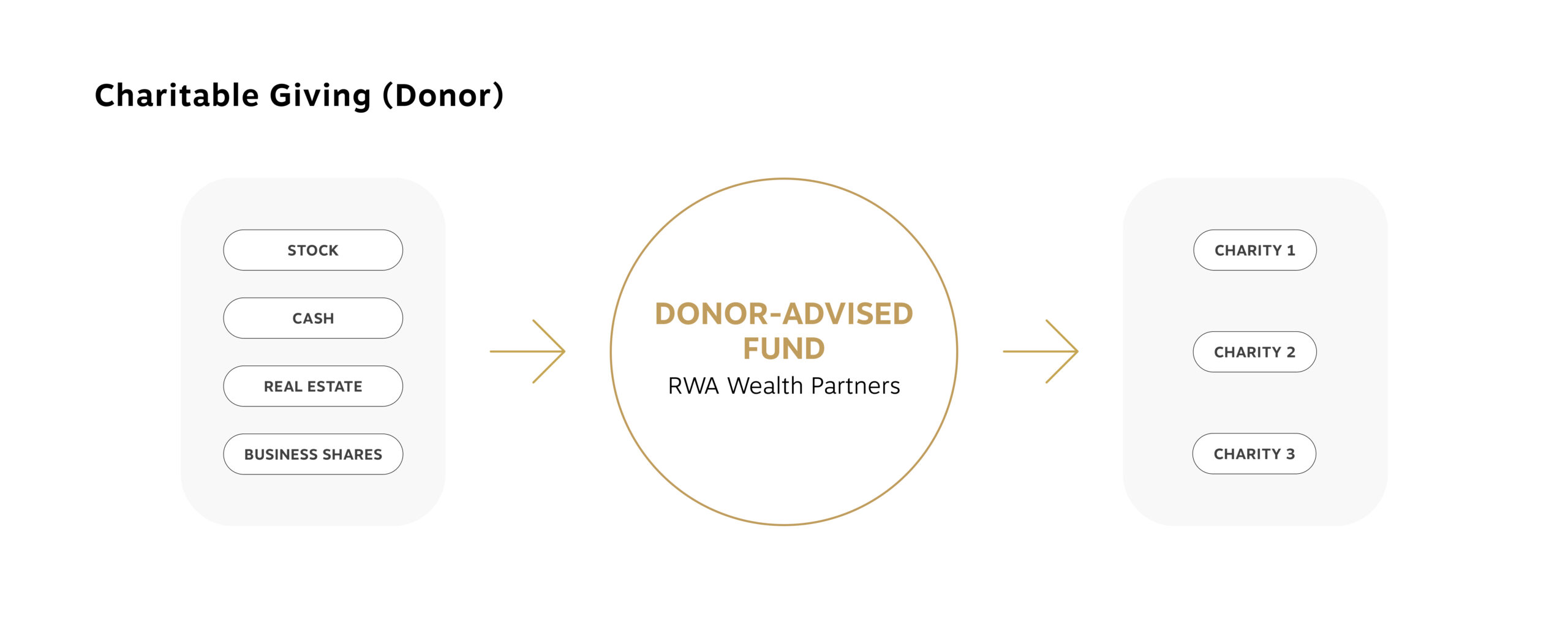

What is a DAF? These funds offer a simple and flexible way to give to your chosen charities while potentially gaining some tax advantages. The fund is a charitable investment account established at a public charity. When you contribute cash, securities or other assets to a DAF, you receive an immediate tax deduction. You then recommend grants from the fund to your favorite charities over time. This structure allows for flexibility in your charitable giving while maximizing tax efficiency.

5 Key Features of DAFs

- Flexible contributions. Donors can contribute cash, stocks, mutual funds, ETFs or other assets at any time and get an income tax deduction for contributions made during the tax year.

- Grant recommendations. You can recommend grants to qualifying charitable organizations at your convenience, spreading contributions over months or years.

- Administrative ease. All transactions and IRS reporting documentation are handled by the DAF sponsor, easing the burden on you. You’ll receive tax-ready confirmations and quarterly investment statements.

- Lower costs. Compared with private foundations, DAFs require less paperwork and have lower administrative costs, making them a more efficient option for charitable giving.

- Letting go. Once assets are contributed to the DAF, a donor relinquishes legal control over those assets.

DAFs are particularly well suited for donors seeking a streamlined and strategic approach to philanthropy and making an impact.

Typical Donor Scenarios for DAFs

Based on our experience managing DAFs for clients, you may benefit from this method of giving if:

- You’re experiencing a high-income year and want to set aside assets for future giving.

- You’re approaching retirement or establishing a DAF during peak earning years.

- You’re seeking to minimize taxes when selling highly appreciated assets.

- You want to simplify gifting your appreciated assets to multiple charities.

- You want flexibility in changing charitable beneficiaries over time.

- You want to engage family members in charitable giving to pass on family values.

- You need time to decide which charities to support.

Seasonal Considerations for Charitable Donations

As we enter the holiday season, some of our clients feel compelled to give back to their communities and support causes they care about. This is often reflected in increased charitable donations during this time. And with the stock market currently at an all-time high, there’s extra incentive to consider making contributions now rather than later.

Why Donate Now?

As mentioned, the stock market is near an all-time high, which means donating appreciated securities now can provide significant advantages and maximize your tax benefits. By donating stocks or other investments that have increased in value, you avoid paying capital gains taxes on those gains while still receiving a tax deduction based on the fair market value of the asset.

Additionally, some clients are taking advantage of “bunching” strategies—making larger contributions in one year to exceed the threshold for itemized deductions. A DAF is an ideal vehicle for this approach, allowing you to take a substantial deduction now while distributing funds over several years.

And lastly, the end of the year often brings increased demand for charitable support as nonprofits seek funding for their programs and initiatives. By contributing now via a DAF, you can respond swiftly to urgent needs while planning your longer-term philanthropic strategy.

Please note that certain types of donations take time to process and may need to wait until next year. But for others, there is still time before the year-end deadline if you start now.

5 Advantages of Donor-Advised Funds

DAFs offer numerous advantages that make them an attractive choice if you’re looking to manage your charitable giving effectively:

- Control over distributions. Unlike direct donations, where funds are immediately transferred to charities, DAFs allow donors to retain advisory control over how and when funds are distributed. This means you can take your time deciding which causes align best with your philanthropic goals.

- Investment options. Many DAFs offer various investment options for your contributions, allowing your funds to grow before being granted out. This feature enhances your ability to give more over time.

- Privacy and confidentiality. Donor-advised funds do not require public disclosure of individual grantmaking activities, allowing you to maintain privacy regarding your philanthropic decisions.

- Reduced administrative burden. Establishing and managing a private foundation can be complex and costly, involving legal fees and regulatory compliance. In contrast, DAFs are much simpler and more cost-effective to set up and maintain.

- Legacy building. DAFs can be structured to allow family members or successors to continue making grants after your lifetime, ensuring that your philanthropic vision endures.

Can a DAF Help You Make a Greater Impact?

As we move further into year-end giving season, DAFs present an excellent opportunity if you’re looking to maximize your charitable impact while enjoying significant tax benefits—especially given recent stock market gains.

By utilizing donor-advised funds, you not only simplify your charitable giving but also retain control over how your contributions are allocated over time—allowing you to create a meaningful legacy while responding effectively to immediate community needs. Whether you’re looking to make an immediate gift or establish a long-term philanthropic strategy, DAFs offer flexibility and efficiency that could align well with your goals.

In this season of giving, consider how a donor-advised fund could enhance both your charitable impact and financial strategy—turning generosity into an even more powerful force for good in our communities.

risk management

Cybersecurity Tips

Cyberfraud is always evolving. With so much sensitive information online and stored within ubiquitous accessories like smartphones, it’s important to be alert to the potential for fraud. Read on for some suggested precautions.

Exercise Caution With Email and Texts

Consider taking measures to minimize the sensitive content in your email account. Avoid sharing financial information unless it is by secure email.

Be vigilant. Look out for suspicious emails and texts. It should raise a red flag if the message:

- Has a strange address or name in the “from” field

- Contains numerous spelling errors or includes odd strings of text

- Asks you to update/confirm your account information by clicking or tapping a link

- Alerts you to an emergency that requires you to send money immediately

These “phishing” emails and texts usually have hyperlinks or attachments. If you are concerned by the contents or suspicious of the message, do not click the link. Clicking on the links can compromise your account, computer or device. Instead, to confirm the contents of the message, go to the provider’s website and log in, or call a service representative using the firm’s publicly listed phone number.

Additionally, it is considered a best practice to install antivirus and antispyware software and apps on all devices and keep them up to date for your protection.

Safeguard Financial Accounts

We urge clients to take several steps to monitor suspicious activity. Review all credit card and financial statements as soon as they arrive or become available online. If you uncover something that raises concern, immediately call the financial institution where the account is held. A phone call is best; it is never a good idea to send account or personally identifiable information by email, chat or any other unsecure channel.

When possible, enable two-factor authentication on apps and accounts. This adds an extra layer of security beyond your password to prevent unauthorized access.

Exercise caution when accessing your online financial accounts from public networks like those in libraries, coffee shops, airplanes or hotel rooms. Cybercriminals can hack into public networks to capture your keystrokes and the passwords they contain. If you must access your accounts via public network, consider using a secure virtual private network (VPN) service that encrypts your data. Also, make sure your home wireless network is password protected. This helps defend against people seeking to gain access to your devices remotely.

Practice Social Media Safety

Personal information about you and your loved ones provides powerful ammunition for scammers to catch you off guard and earn your trust. Protect your Social Security number (even the last four digits), birth date, home address and home phone number carefully. Refrain from posting social media announcements about upcoming vacations, births, children’s birthdays or the loss of a loved one. Never underestimate the lengths cybercriminals will go to in order to learn your habits and critical facts about you.

Vigilant Together

If you suspect you are the victim of cyberfraud or have concerns your identity or device has been compromised, please speak to your advisor so we can review the accounts we manage for you and take further action to safeguard them.

Additionally, please know our procedures, which include calling to verbally confirm instructions, using encryption on email messages, and verifying personal information, are intended to protect you and your information. We’re in this together, and as the threats evolve, we’ll be partners in defending your information, just as we’re partners in building your financial and wealth plan.

The information set forth in this communication is presented by RWA Wealth Partners, LLC (“RWA”). The contents are for informational and educational purposes only and are not intended as investment, legal or tax advice. Please consult with your investment, legal or tax advisor concerning any specific questions you may have. Past results are not indicative of future performance. The historical return of markets generally and of individual asset classes or individual securities may not be an accurate predictor of future returns of those markets, asset classes or individual securities. RWA does not guarantee the accuracy and completeness of any sourced data in this communication.

© 2024 RWA Wealth Partners, LLC. All Rights Reserved.