This year was a strong one for the stock market, but it didn’t start out that way. In this article, we will highlight some of the surprises we saw and share our latest thinking about the markets, inflation, interest rates and the overall economy. Most importantly, we’ll explain how this all informs our thinking about your portfolio as we head into 2025.

Stock Market Expectations vs. Reality

Do you remember what Wall Street and the media were projecting for the stock market at the beginning of 2024? Many predicted it would fall this year, on average, by about 1%.

The market defied these expectations as the economy shrugged off a potential slowdown and consumers kept on spending despite higher prices, which allowed businesses to pass along higher input costs and post record earnings results. And now, as we approach the end of the year, the S&P 500 is holding above 6,000, trading near its all-time high, having gained more than 28% this year through mid-December.  Remember this year’s gain comes on top of last year’s impressive showing. You can see in the chart below how, over the last six calendar years, except for 2022, the stock market delivered performance well in excess of its historical average, which is about 10% per year.

Remember this year’s gain comes on top of last year’s impressive showing. You can see in the chart below how, over the last six calendar years, except for 2022, the stock market delivered performance well in excess of its historical average, which is about 10% per year.  So what does this mean for you? We want you to remember this example when you start to hear predictions for 2025. These Wall Street firms have a job to do, but their forecasts are often geared toward grabbing headlines and have no bearing on your individual planning and investment goals. This is why we advise you to focus on your personal circumstances and discuss any concerns about your current financial plan and investments with your advisor, who can tailor recommendations to your individual needs.

So what does this mean for you? We want you to remember this example when you start to hear predictions for 2025. These Wall Street firms have a job to do, but their forecasts are often geared toward grabbing headlines and have no bearing on your individual planning and investment goals. This is why we advise you to focus on your personal circumstances and discuss any concerns about your current financial plan and investments with your advisor, who can tailor recommendations to your individual needs.

But back to the market, what happened this year to cause such a disconnect from expectations?

Of course there are many factors, but if there was one big lesson to take away from the stock market in 2024, it was that optimism is typically rewarded over the long term. There were so many reasons to lose confidence this year or to feel uncertain about what lies ahead, but companies are dynamic entities that can adjust to varying conditions, and we saw this play out over the last 12 months.

So, why did the stock market do so well this year? In a word, earnings.

Earnings Tell the Tale

The chart below shows earnings growth for S&P 500 companies over the last 11 years, illustrating how earnings supported market gains. This year, earnings per share (EPS) are estimated to have grown by about 9%. And expectations are even higher for next year.  What’s driving this earnings growth? There are two big trends that have created the most value for market participants during this bull run: Artificial intelligence (AI) and GLP-1 drugs like Ozempic, Wegovy and others.

What’s driving this earnings growth? There are two big trends that have created the most value for market participants during this bull run: Artificial intelligence (AI) and GLP-1 drugs like Ozempic, Wegovy and others.

AI was a difference maker this year and we expect this trend to continue going forward. While a large portion of the return was captured by companies like Nvidia, we may see other firms benefit and come to the forefront as this next chapter of the AI story unfolds.

The other big trend was the popularity of the GLP-1 class of drugs. The growth of this market has been remarkable and was largely driven by increasing demand for medications that help people manage obesity and Type 2 diabetes. The rapid uptake by consumers and hopeful results from these drugs (which are addressing a critical public health issue for millions of people) helped contribute to strong results for companies like Novo Nordisk and Eli Lilly, among others.

These two trends fed into one of the biggest stories of the year in the stock market—the dominance of large-cap growth stocks. But more recently, there’s been a change in the market’s leadership, and we’ve seen it broadening out to include other areas. This is benefiting investors with diversified portfolios and we think this could continue into next year.

What About Interest Rates?

Now let’s shift gears and talk about the bond market and interest rates, which, along with earnings, set the tone for the economy and markets.

Let’s start with a quick review of where we are with inflation. This chart shows three inflation indicators going back to 2022. One is the headline consumer price index (CPI), which has been reined in the most, down to 2.7% year over year. The other two indicators are the core services number (which includes a whole host of services from haircuts to landscaping) and shelter. Both of these CPI components remain stubbornly high at 4.6% and 4.7%, respectively.  The punchline is the Federal Reserve made a lot of progress in bringing inflation down, but that progress has recently stalled, particularly in these areas where inflation is historically sticky. This makes it more difficult for the Fed to bring inflation to its target level without causing an economic disruption.

The punchline is the Federal Reserve made a lot of progress in bringing inflation down, but that progress has recently stalled, particularly in these areas where inflation is historically sticky. This makes it more difficult for the Fed to bring inflation to its target level without causing an economic disruption.

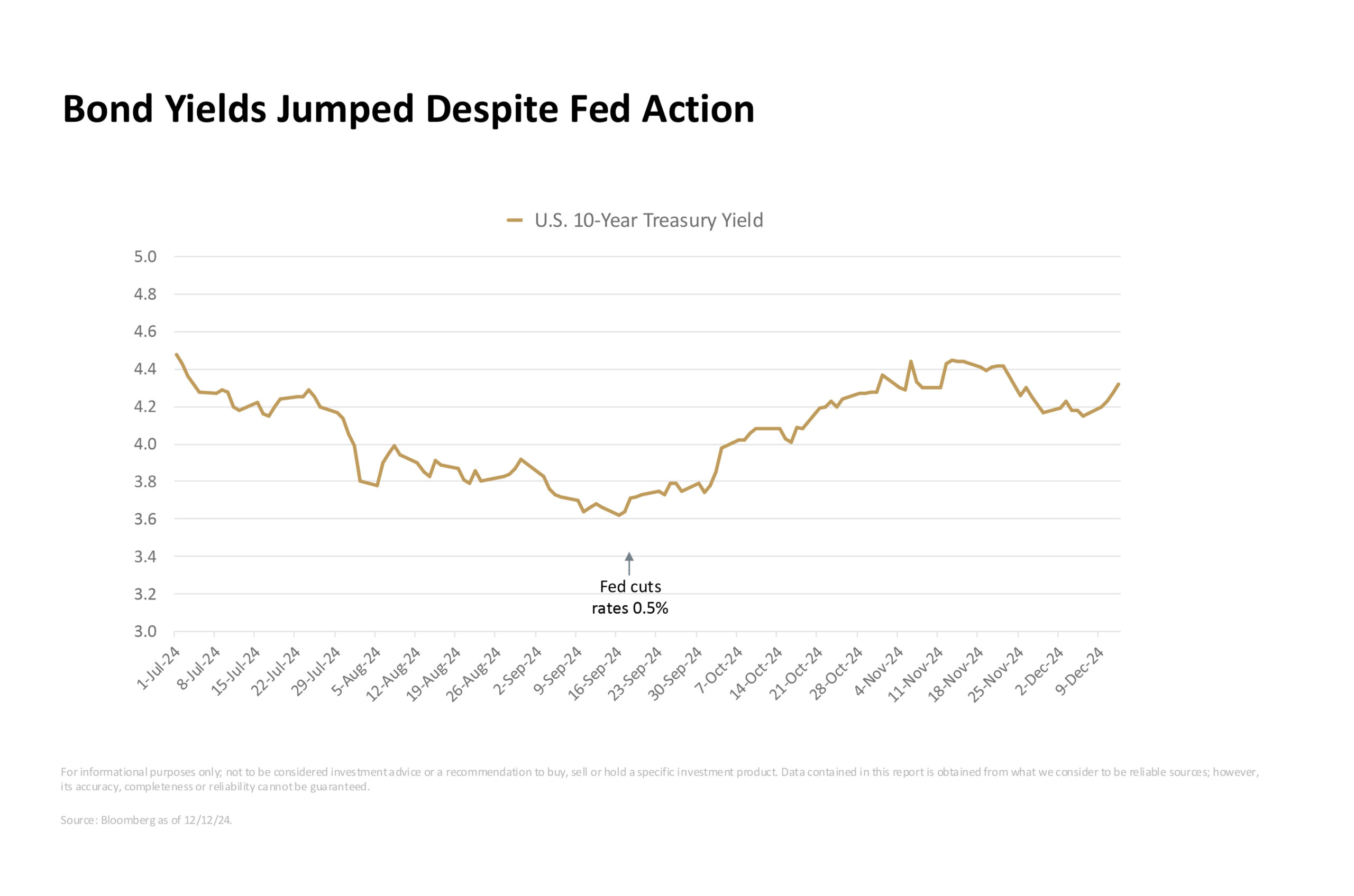

So, what does that mean for the bond market and interest rates? There’s something rather uncharacteristic going on in the bond market.

A look at how the 10-year Treasury note’s yield changed over the year is instructive. We’ve highlighted when the Fed cut rates by 50 basis points back in September. Despite the Fed lowering short-term interest rates, long-term interest rates—defined here by the 10-year Treasury—have risen, and by a lot. It may seem counterintuitive, but the bond market (like most investments) is forward-looking. So while the Fed has cut rates multiple times, the market isn’t convinced that it’ll continue to do so in 2025.  We think bonds could present an opportunity to pick up some meaningful return, which hasn’t been the case for many years. In the chart below, you can see 10-year government bond yields across Canada, France, Germany, Italy, Japan, the U.K. and the U.S. Currently, the U.S. is just a tick below the U.K. As a result, global demand for U.S. Treasurys has been robust.

We think bonds could present an opportunity to pick up some meaningful return, which hasn’t been the case for many years. In the chart below, you can see 10-year government bond yields across Canada, France, Germany, Italy, Japan, the U.K. and the U.S. Currently, the U.S. is just a tick below the U.K. As a result, global demand for U.S. Treasurys has been robust.  We think the recent rise in long-term rates offers you another opportunity in the bond market. And depending on your situation, this might potentially be a better strategic allocation choice than cash or short-term T-bills. Discuss this with your advisor directly to see what is best for your portfolio.

We think the recent rise in long-term rates offers you another opportunity in the bond market. And depending on your situation, this might potentially be a better strategic allocation choice than cash or short-term T-bills. Discuss this with your advisor directly to see what is best for your portfolio.

What’s the Fed’s Next Move?

After this week’s Federal Open Market Committee meeting, where the central bankers cut rates by 0.25% to a range of 4.25% to 4.50%, investors are speculating about what the central bank will do next. Will the Fed pause because some aspects of inflation remain stubbornly high and the economy appears to be in better shape than anticipated? Or will it keep cutting rates to avoid contributing to a potential slowdown next year?

The answer is this: The economy will, and should, dictate the path forward on rates, and Chair Jerome Powell said as much following the December policy meeting. Today, the U.S. economy remains the strongest in the world.

Let’s look at the same group of countries we considered above but with their estimated GDP growth added in. You can see the U.S. is delivering considerably better results along with one of the highest sovereign yields.

With the election behind us and a new presidential administration preparing for office, it’s time to review how campaign trail promises could influence the economy if enacted. Up first is immigration.

President-elect Trump has said one of his administration’s highest priorities is to deport unauthorized immigrants living here. We examine potential economic effects and investment considerations, focusing solely on market implications rather than the political or humanitarian aspects of such a policy.

Historical Precedent and Recent Experience

Historical precedent, while limited, offers some insight. In 1954, under President Dwight Eisenhower, the federal government carried out a military-style immigration enforcement initiative that sent more than 1 million people across the border to Mexico in its first year. Affected agricultural regions saw significant production disruptions as a result. The program continued until 1962, when it was defunded due to its failure to prevent illegal immigration and public outcry over the number of U.S. citizens swept up and deported during enforcement actions.

The most relevant modern example is the Obama administration’s Secure Communities program, which resulted in more than 400,000 deportations between 2008 and 2014. When these workers were removed from the labor force (through both direct deportations and indirect effects), approximately 44,000 U.S.-born workers lost their jobs.

Contrary to expectations, employers did not simply replace deported workers with U.S. citizens. Instead, many businesses either reduced operations or invested in automation, leading to an overall decrease in employment opportunities. The program also impacted child care services, reducing the availability of care workers and causing some college-educated mothers to exit the formal labor market.

These real-world examples suggest that market adjustments to deportation policies tend to be complex and often produce unintended consequences across multiple sectors. Rather than simple worker substitution, the evidence points to broader economic contraction in affected industries and regions.

Scale and Timing

In this analysis, we consider two potential implementation scenarios: A one-time mass deportation and a gradual approach over approximately 11 years. According to the American Immigration Council, the one-time scenario would cost $315 billion in government spending, while the gradual approach would total $968 billion. Both tactics would remove approximately 7.5 million people from the labor pool, representing 4.6% of the current workforce.

GDP projections vary by source and scenario. The Peterson Institute for International Economics estimates impacts by 2028 ranging from 1.2% to 7.4% below a scenario with no immigration reform, depending on deportation scale. The American Immigration Council estimates an annual GDP reduction of 4.2% to 6.8% ($1.1 trillion to $1.7 trillion in 2022 dollars).

Market Implications

Under either the fast or gradual approach, labor markets would face disruption across several key sectors.

Construction would lose 14% of its workforce, while agriculture would lose up to 33% in key roles. Companies in these sectors could face higher labor costs and reduced operational capacity, potentially impacting earnings. Manufacturing and transportation companies would also face staffing challenges, particularly in regions with high immigrant populations. This could increase production costs and create or exacerbate preexisting supply chain issues. Companies will likely pass these costs on to consumers, contributing to higher inflation for goods and services in affected industries.

The real estate market would feel effects from multiple directions. Nearly 40% of undocumented immigrant households own their homes—the removal of 1.6 million homeowners from the market could create inventory pressures in certain regions while simultaneously reducing demand for rental properties. Property values in heavily impacted areas might face downward pressure, and new construction could slow significantly due to labor shortages.

Consumer spending could contract by an estimated $257 billion annually, affecting multiple sectors of the economy. While consumer staples might prove relatively resilient, companies focused on discretionary goods could see more significant revenue declines. Local businesses in affected regions would likely face the strongest headwinds.

Banks with significant exposure to affected regions or industries might see increased mortgage default risk, reduced demand for new loans and higher small business loan risks. Some institutions might also experience deposit outflows as deportees are relocated.

Investment Considerations

Investment Considerations

Sectors like health care, technology and utilities, which rely less on immigrant labor or domestic consumption, could offer more stability during the implementation period, as could export-oriented companies. Companies involved in automation, robotics, security technology and government services contracting may see increased growth potential. The U.S. bond market could face pressure from increased government spending.

Markets with high immigrant populations, particularly in California, Texas and Florida, could experience outsized economic effects due to the loss of lower-cost labor.

The short-term outlook suggests increased market volatility during policy implementation. The projected GDP reduction indicates potential for broad market impact.

Risk management becomes particularly important in this environment, especially for portfolios with significant exposure to affected industries and regions. Diversifying among U.S. sectors and international stocks and strategically allocating to higher-growth-potential industries would make sense in this scenario.

Looking Forward

The implementation of mass deportation policy would create significant market adjustments across multiple sectors. While some areas of the market face clear challenges, others might find opportunities in the changing economic landscape. On top of that, many questions remain as to how the government will manage the logistics and fiscal requirements for the scenarios covered above. As more details become available, we’ll incorporate the policy’s implications into our economic and investment management outlook and be ready to adjust your portfolios and plans as needed.