Potential Turbulence Ahead

The biggest foreseeable challenges on the horizon for investors are the U.S. election this fall and the possibility of a broadening conflict in the Middle East.

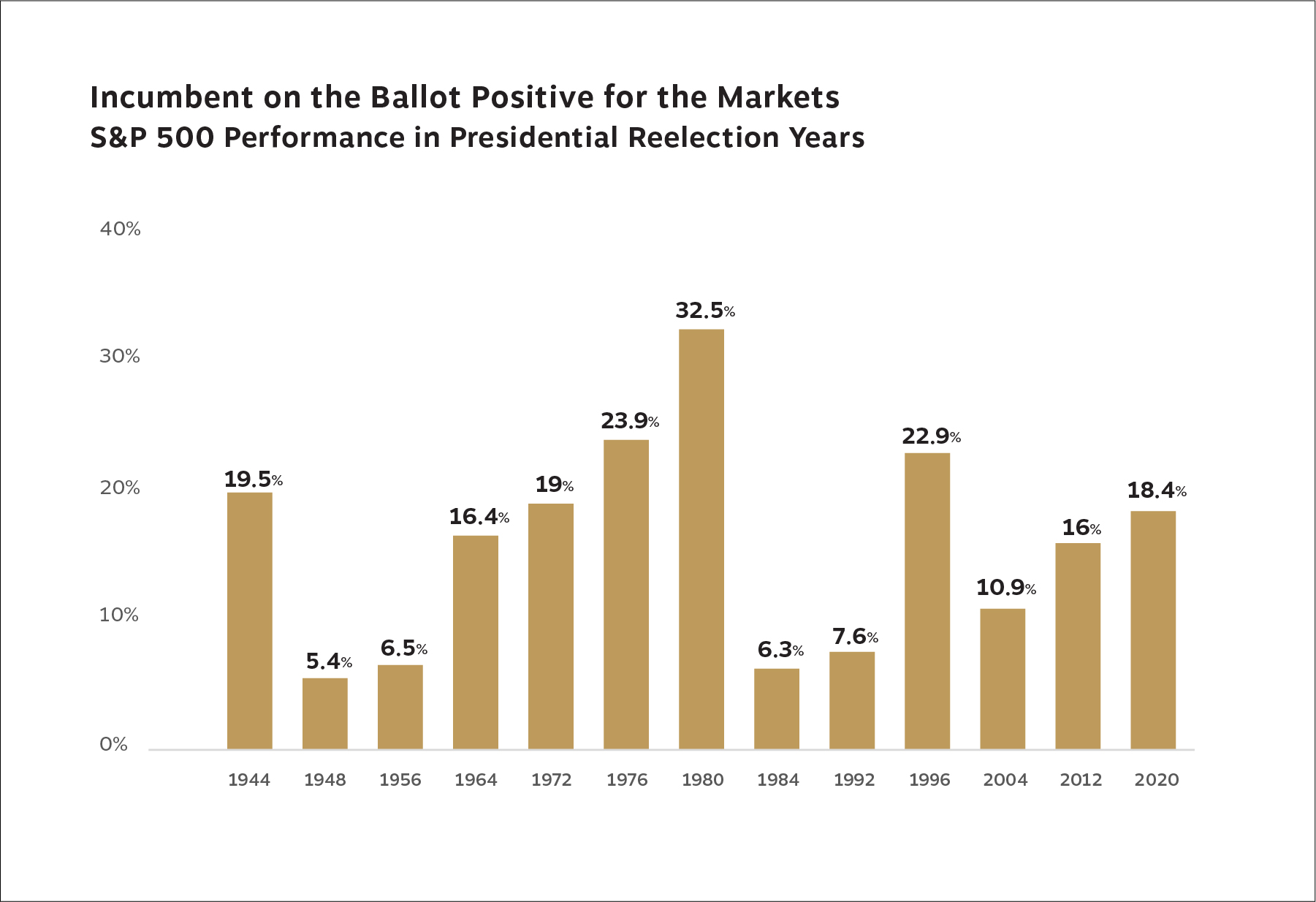

The chart below offers some perspective on what happens during election years when the incumbent is on the presidential ballot. You can see that stocks have gained in the 13 such instances since 1944. As election season becomes more emotionally charged and widens divisions across the political spectrum, our job is to filter out the noise and continue to act in your best financial interest.

We’ll have more on this topic in the months ahead, but remember that making portfolio allocation decisions based on politics and elections carries a significant risk of derailing your plans. Your goals, income requirements, lifestyle needs and comfort with investment risk comprise the soundest foundation on which to build an enduring wealth strategy. Please speak to your advisor if you have concerns about election outcomes as they relate to your financial plan.

Gauging Consumers, the Job Market and GDP

The labor market is strong, and low unemployment supports consumer confidence. The March retail sales report showed an increase of 0.7% last month, higher than the 0.4% expected. We are not a nation of savers: When the job market is near full employment and consumers are confident, they spend. That spending supports our economic growth, as roughly 70% of U.S. GDP is tied to consumption.

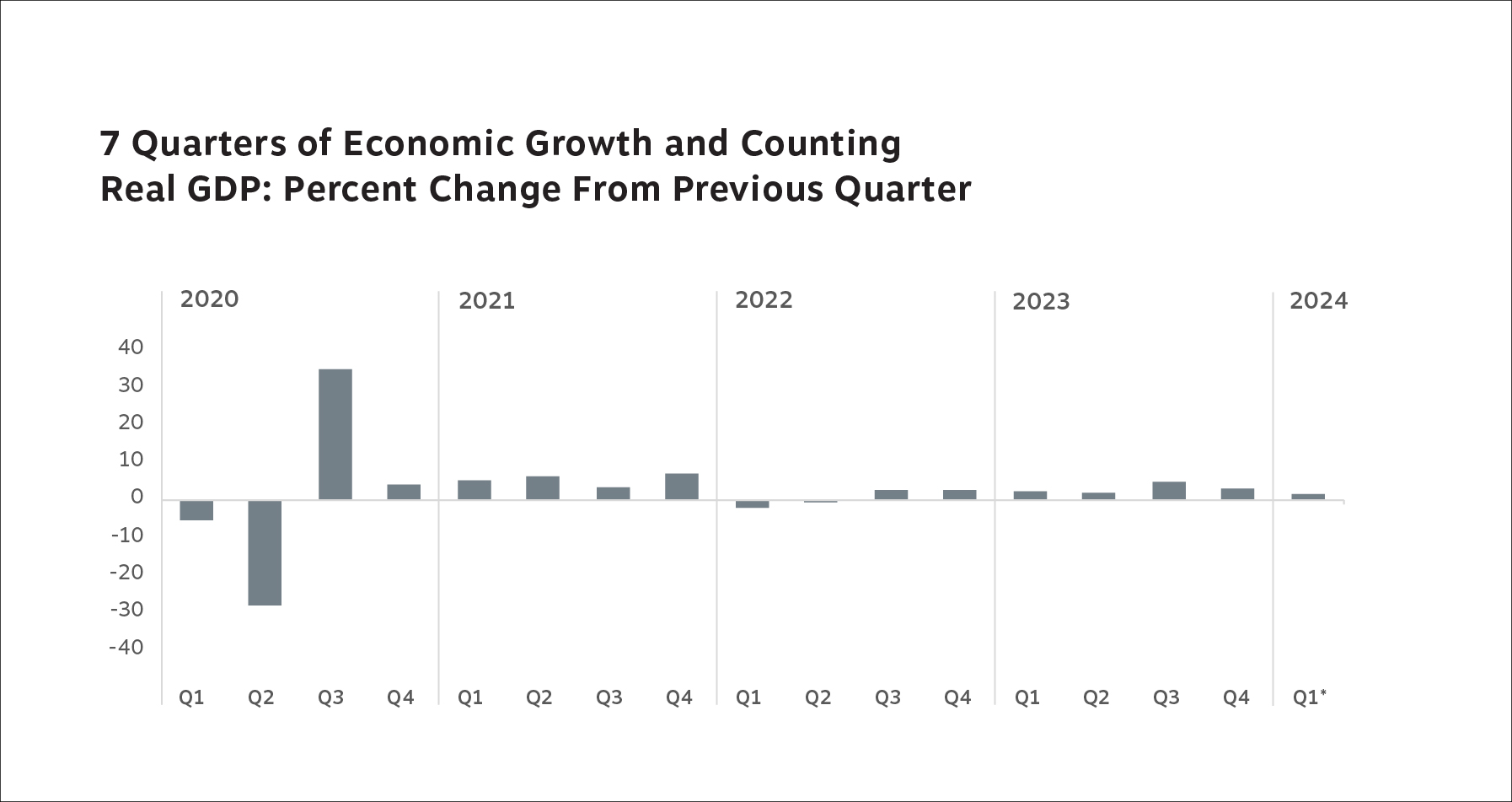

And the economy has been growing, though some signals are mixed. GDP grew at a 3.4% annual pace over the last three months of 2023 and 1.6% in Q1 2024 according to the advance estimate from the Bureau of Economic Analysis—lower than expected. While concerns about an inverted yield curve, stubborn inflation and the housing market linger, we’ve seen more evidence of a soft landing for the economy than we have of a recession. Is a recession still possible? Of course. Is a recession probable? Not anytime soon.

Plotting Federal Reserve Policy

We put the Federal Reserve square in our sights at the beginning of the year, anticipating that investor reactions to the central bank’s fight against inflation would sway the market in 2024. And that’s what we’ve experienced.

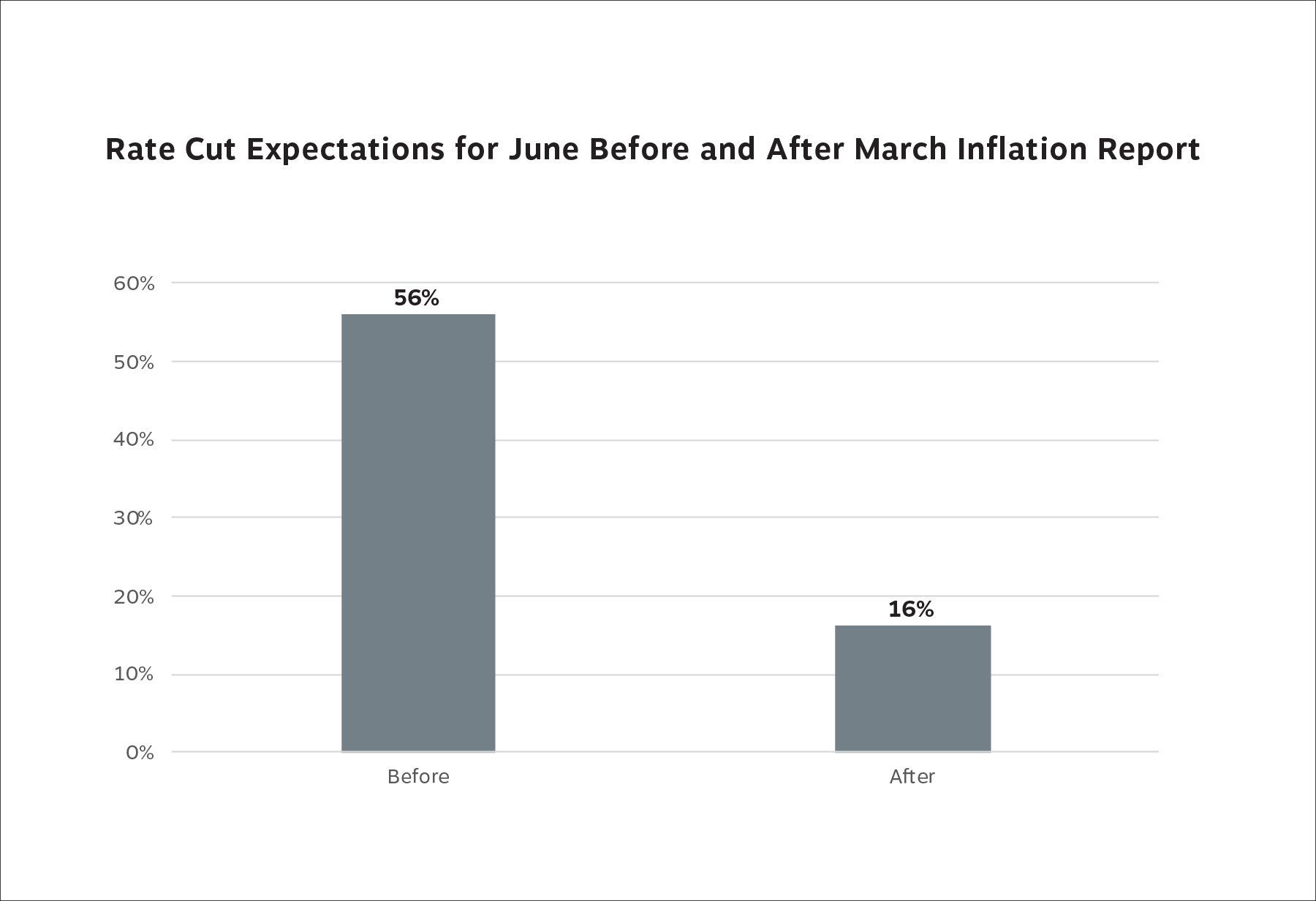

The surprise March inflation report is a recent example. Consumer prices rose 3.5% year over year, rattling analyst assumptions that inflation would trend lower and the Fed would cut interest rates in June. After the report, rate policy expectations changed, and stocks pulled back.

The chart below shows expectations for a 25-basis-point rate cut on April 9 (the day before the March inflation report) and where they stood on April 10 (after the inflation surprise). Confidence in a rate cut fell 40% in mere hours. Short-term moves like these (and the accompanying negative 1% one-day reaction in the stock market) make for snappy media sound bites, but they’re unreliable long-term investment indicators.

Instead, it’s our longstanding belief that earnings and interest rates give the strongest indications of where stocks are heading.