The passage of the One Big Beautiful Bill Act (OBBB) ushers in sweeping changes to taxes that will frame legacy planning and wealth strategy for years to come. Signed into law on July 4, 2025, the OBBB not only makes permanent many of the provisions of the Tax Cuts and Jobs Act (TCJA) from 2017, but it also introduces new nuances and strategic opportunities that may help preserve and grow your wealth.

Will the changes in the new tax law work in your favor? Is there more you could be doing to enhance your wealth strategy?

Below is our analysis of what we think may be most consequential for you and your family.

Permanent Individual Rate Structure and Standard Deduction

Income tax rates: Rates of 10%, 12%, 22%, 24%, 32%, 35% and 37% are now permanent and will be adjusted for inflation annually. This move averts the reversion to higher, pre-TCJA rates that was scheduled to hit after 2025.

Income tax rates: Rates of 10%, 12%, 22%, 24%, 32%, 35% and 37% are now permanent and will be adjusted for inflation annually. This move averts the reversion to higher, pre-TCJA rates that was scheduled to hit after 2025.- Standard deduction: This is permanently increased and indexed for inflation, with 2025 deductions set at $15,750 (single), $31,500 (joint) and $23,625 (head of household). Personal exemptions are gone for good.

- Alternative minimum tax (AMT): Exemption amounts and phase-outs are extended permanently, with key thresholds adjusted upward for higher earners.

State and Local Tax (SALT) Deduction Expansion With a Catch

Deduction cap: The SALT deduction cap rises from $10,000 to $40,000 per household beginning in 2025. This cap increases 1% annually through 2029, then reverts to $10,000 in 2030.

Income phaseouts: The $40,000 cap begins phasing down once modified adjusted gross income (MAGI) exceeds $500,000, reducing by 30% of the excess, but it does not phase down below the original $10,000 limit; $600,000 is where it fully phases down to $10,000.

Planning nuances:

- Deduction includes state income, real estate and personal property taxes.

- There are no changes to pass-through entity tax workarounds.

- High-income taxpayers in states like California, New York and Massachusetts stand to benefit most.

Strategic Shifts in Credits and Charitable Giving

- Child tax credit: This is permanently increased to $2,200 per qualifying child, indexed to inflation, with unchanged phaseout thresholds: $200,000 (single) and $400,000 (joint).

- Child and dependent care credit: This limit is raised from 35% to 50% of qualifying costs, with phaseouts ensuring no credit falls below 35%.

- Above-the-line charitable deduction: From 2026, this is available for non-itemizers at $1,000 (single) or $2,000 (joint). For itemizers, only charitable donations above 0.5% of AGI are deductible, and the value of itemized deductions is limited to 35% for those in the 37% bracket.

Senior and Family-Focused Opportunities

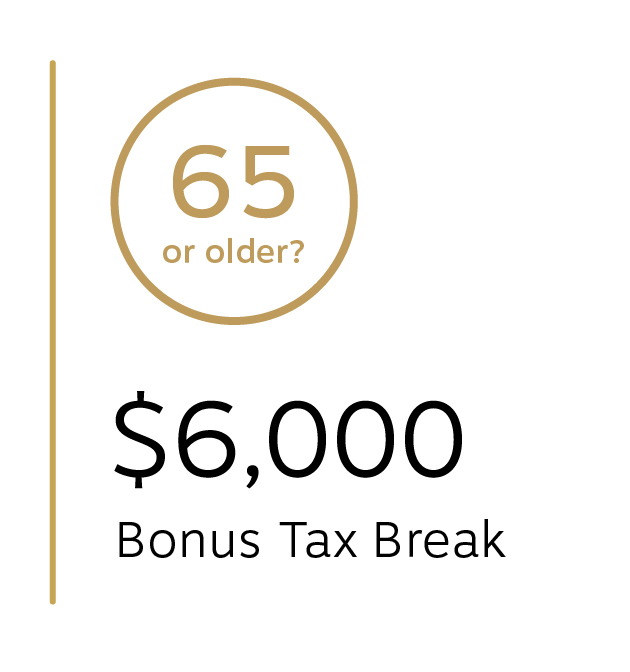

Senior deduction: This is a temporary (2025–2028) additional $6,000 (single) or $12,000 (joint) deduction for taxpayers 65 and older. It phases out at $75,000 (single) and $150,000 (joint) MAGI.

529 plan enhancements:

- Starting in 2026, qualified education expenses expand to include K–12 tutoring, homeschooling, workforce training and special needs therapies.

- K–12 tuition limit climbs from $10,000 to $20,000 per year.

Trump child savings accounts:

- For children under 18 (or under 8, depending on the provision), parents and family may contribute up to $5,000 post-tax per year, indexed for inflation.

- No distributions are allowed until the calendar year in which the child turns 18.

- Investment is limited to broad U.S. stock index funds; withdrawals follow graduated age milestones, with tax treatment varying by use and timing.

Estate, Gift and Business Owner Tax Provisions

- Estate and gift tax exemption: From 2026 onward, this will be permanently set at $15 million (single) and $30 million (joint), indexed for inflation. This will prevent a sharp drop-off after 2025 and support multigenerational transfer strategies.

- Qualified business income (QBI) deduction: The 20% deduction for pass-through entities is now permanent, with phaseouts for professional service income at $75,000 (single) and $150,000 (joint).

- Miscellaneous deductions: Many itemized deductions previously subject to the 2% AGI limitation (e.g., investment management, tax preparation, unreimbursed business expenses) remain disallowed.

Specialized Deductions and Phaseouts

- No tax on tips and overtime: For 2025–2028, above-the-line deductions for up to $25,000 in tips and $12,500 ($25,000 joint) in overtime will apply, phasing out for high earners.

- Car loan interest: This is deductible up to $10,000 per year (2025–2028) for new vehicles assembled in the U.S., with strict income phaseouts.

- Mortgage interest: The $750,000 principal cap for deductible interest is made permanent. Home equity loan interest generally remains deductible for home improvement expenses.

Other Key Changes Impacting Wealth Planning

- Qualified Opportunity Zone (QOZ) program: This is indefinitely extended, with new tranches of QOZs to be designated every 10 years, creating planning opportunities for capital gains management.

- Clean energy and electric vehicle credits: Most residential clean energy credits, including those for solar, heat pumps and EVs, sunset in 2025. The EV credit expires on Sept. 30 and the home energy credit expires on Dec. 31. A few commercial clean energy incentives remain.

- Pease limitation removal, but new cap: While the Pease limitation (AGI-based reduction of itemized deductions) is gone for good, high earners face a 35% cap on the marginal tax benefit of itemizations.

- 529 plan and QOZ expansion: This permits additional uses and higher contribution limits for future-facing educational and impact investments.