This philosophy is not hard to grasp, but you have a plethora of options for putting it into place, each of which can be tailored to your specific goals. Let’s look at a few of the most popular choices, broken down by three broad objectives: transferring wealth to your family, philanthropy and a mix of the two.

Family Wealth Transfer

Annual exclusion gifts. The simplest approach is direct gifting, using the annual gift tax exclusion ($19,000 per recipient in 2025). Married couples can combine their exclusions, allowing for significant tax-free transfers.

Direct payment of medical and education expenses. You can make unlimited payments directly to medical providers or educational institutions on behalf of others for qualified expenses without incurring a taxable gift or affecting your $19,000 gift exclusion.

Gifts of lifetime exemption. The lifetime exemption is the total amount of money or property that an individual can transfer to others during their lifetime as gifts or at the time of their death without incurring any federal or estate tax.

In 2025, an individual can gift up to a lifetime exemption of $13.99 million. The exemption is calculated per person, so a married couple has double that. Gifting between spouses is unlimited and usually doesn’t require a gift tax return.

If you have an estate approaching or above the $14 million level as an individual or $28 million as a couple, making gifts today can be an especially powerful wealth transfer technique. The future growth of those gifted assets occurs outside of your taxable estate. Gifts can be made directly to loved ones or into trusts for their benefit.

Grantor retained annuity trusts (GRATs). GRATs provide a way to transfer appreciation on assets to the next generation while retaining an income stream for yourself. This vehicle is particularly effective in low-interest-rate environments and for assets expected to appreciate significantly.

Charitable Giving Strategies

Donor-advised funds (DAFs). DAFs offer immediate tax benefits, have the potential to grow over time and allow you to recommend grants to charities over time. They’re an excellent way to involve family members in philanthropic decisions and create a lasting legacy of giving.

Private foundations. For substantial charitable commitments, private foundations offer maximum control and visibility. They can employ family members and create a permanent family legacy while supporting chosen causes.

Hybrid Approaches

Charitable lead trusts (CLTs). CLTs provide current income to charities while ultimately transferring assets to family members at reduced gift tax values. This structure benefits both charitable causes and family beneficiaries.

Charitable remainder trusts (CRTs). CRTs combine charitable giving with family wealth transfer. They provide income to family members for a period of time, with the remainder going to charity. This structure offers current tax benefits while benefiting both family and charitable beneficiaries.

Crafting Your Plan

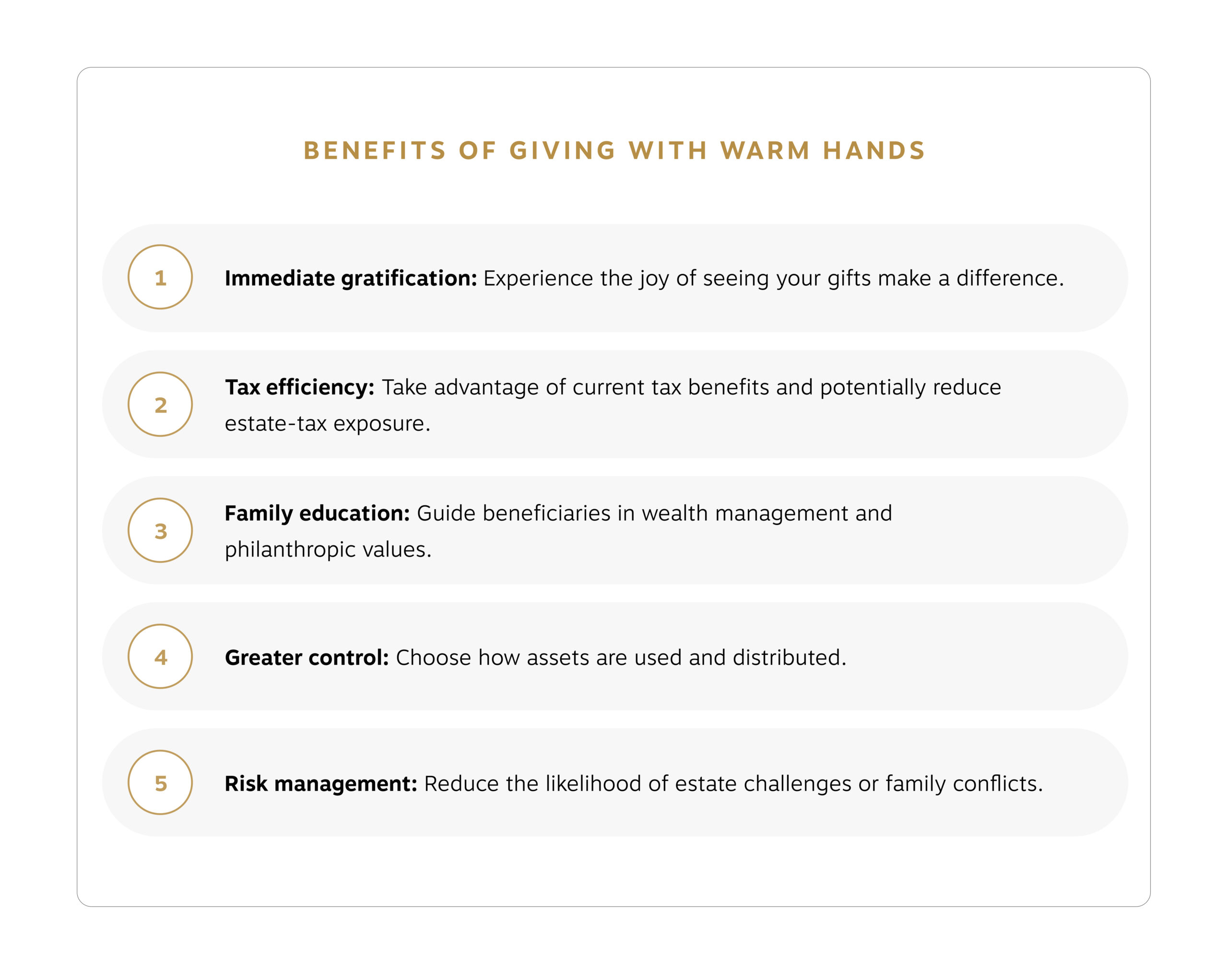

The key to successful lifetime giving is careful planning that aligns with your overall financial goals. Remember that different giving vehicles offer varying levels of control, tax benefits and complexity—some will require assistance from a lawyer. Your team can help guide you in selecting and implementing the strategies that best fit your situation.

By giving with warm hands, you can craft a legacy that benefits both family and society while maintaining the flexibility to adjust your approach as circumstances change. Contact your team to learn more and get started.