Are Stocks Just a Cold Weather Accessory?

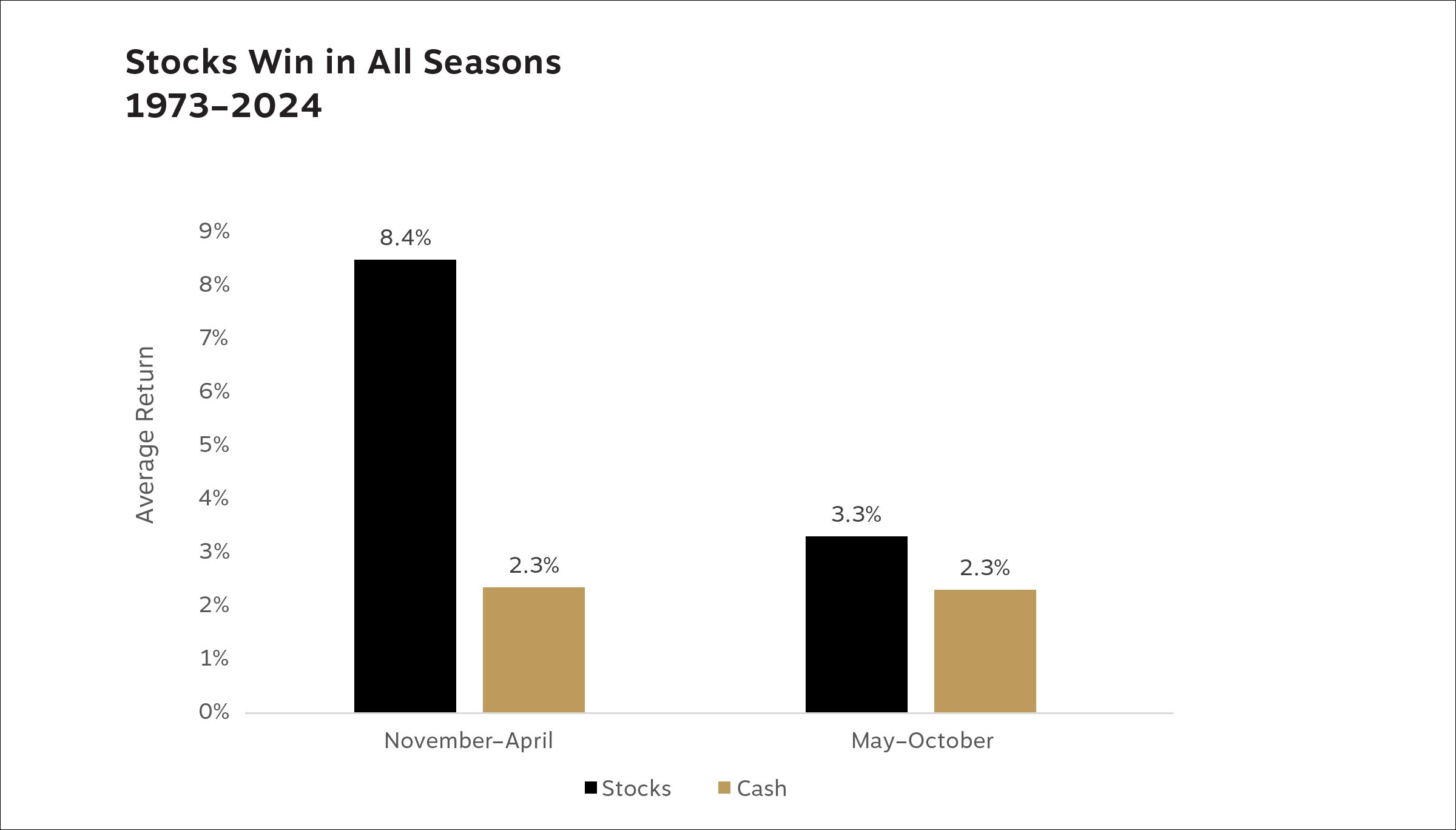

Surprise! At first blush, the claim that stock performance from November through April is better than from May through October is grounded in fact. Since November 1973, the average six-month total return from fall to spring has been 8.2% for stocks (represented by the S&P 500 index), compared with a 3.3% average from May through October. However, that doesn’t reveal the full picture.

Unfortunately for proponents of selling in May, substituting cash for stocks has not been a winning move. Over the last 50 years, the average return for cash (represented by three-month Treasury bills) during the May–October period has been 2.3%, a full percentage point less than stocks. For the full November 1973 to April 2024 period, the sell-in-May strategy generated a 10.5% annualized gain while stocks had an 11.1% return.

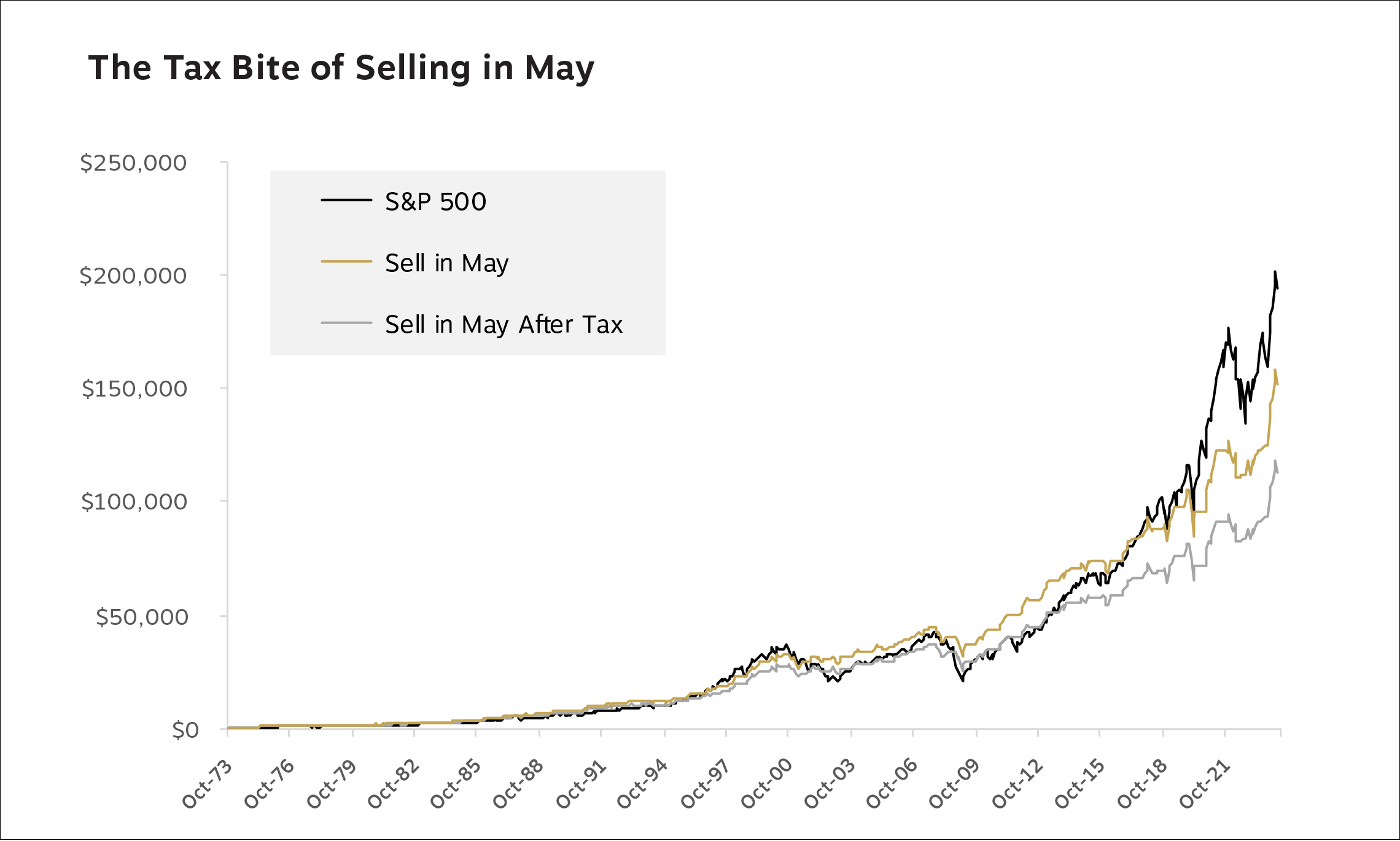

That seems like a small difference, but it adds up over 50 years: $1,000 invested in a sell-in-May strategy grew to just over $158,000. But holding only stocks turned that $1,000 into more than $201,000. Put another way, following a sell-in-May scheme deprived you of 22% of your potential gains.

Don’t Forget About Uncle Sam

If you apply the sell-in-May strategy to a taxable account, factoring in the impact of short-term capital gains taxes for each spring’s stock sale, it puts you even farther behind. Using this strategy would generate an annualized return of 9.9%, compared with 11.1% for buying and holding stocks. The end value after 50 years is just 58% of what you’d have pretax from a buy-and-hold stock strategy. The chart below shows hypothetical growth of $1,000 following the different strategies and the large discrepancy in ending values.

Does Selling in May Ever Work?

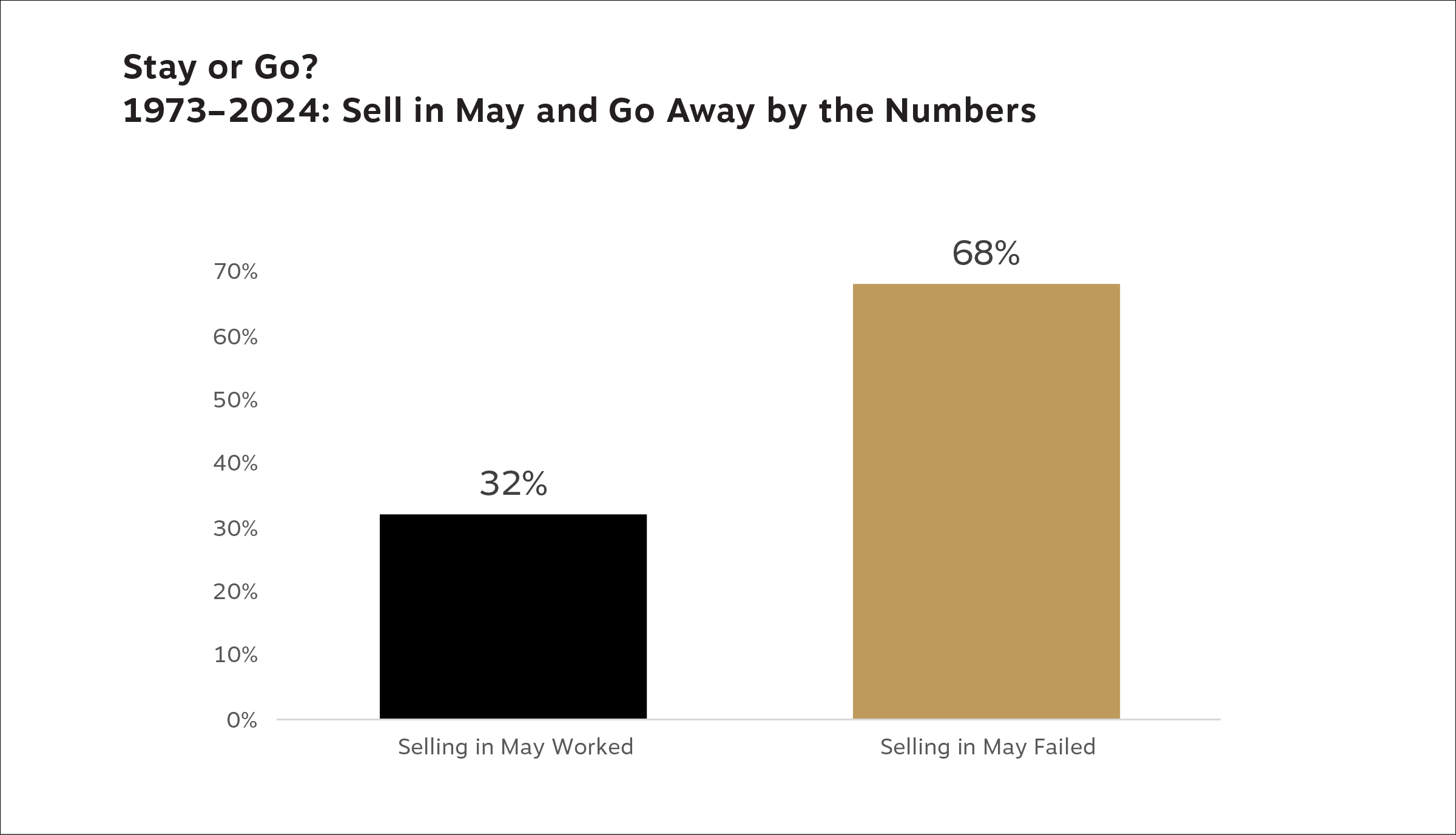

As is often the case with myths, there is a thread of truth woven into the tale. We already know that stocks typically perform better in the cooler months. And there have been years when selling in May would have paid dividends. In fact, it’s worked for the last two years in a row.

But don’t get your hopes up for a threepeat—it’s unlikely. Those two successful instances were preceded by 10 consecutive years when the strategy failed (eight of which are shown in the table above). And over the 50 years we analyzed, the strategy only worked 16 times, or 32% of all years. The other 68% of the time, you would have been better off holding stocks.

So, while it may be time to put your parka away and pull out sundresses and summer slacks, leave the sell-in-May-and-go-away strategy in the closet. Time has shown that stocks are more fashionable for long-term investors than cash, no matter the season.