When markets become turbulent, even experienced investors can feel uneasy watching their portfolio values fluctuate. Larger portfolios often mean larger dollar swings during market drawdowns, which can be tough to bear. Yet building and preserving wealth requires maintaining perspective and discipline, especially during uncertain times. That’s why it’s important to work with your advisor on a game plan that won’t let market declines “bust your bracket.”

Understanding Market Corrections: Downturns Are Normal

In mid-March, the S&P 500 index (a benchmark for large U.S. company stocks) fell into correction territory when it declined 10% from its prior high. But corrections—periods when investments drop in value temporarily by 10% or more—are not unusual events. They’re regular features of healthy markets. As you can see in the chart below, the data tells a compelling story: Despite experiencing average drops of 14% during a given calendar year, the S&P 500 has delivered positive annual returns in 34 of the past 45 years.

This pattern is striking. Even in years with positive returns, investors regularly endured significant declines along the way. In 2009, for example, the market dropped 28% at one point before finishing with a 23% gain. In 2020, a dramatic 34% decline during the pandemic still resulted in a 16% gain by year’s end.

Having this historical perspective helps transform alarming headlines into isolated episodes within a broader wealth-building journey.

Spreading Your Investments: The Power of Diversification

We believe a well-balanced portfolio of stocks and bonds remains the cornerstone of successfully investing through market volatility. That’s why we craft personalized portfolios attuned to your risk comfort and long-term goals. We base our approach on the following principles:

True diversification means portions of your portfolio will occasionally move in different directions—when one area underperforms, another may outperform. This isn’t a flaw but rather evidence that your strategy is working exactly as designed to help you weather market volatility.

Rebalancing: Turning Market Swings Into Opportunities

Periodically rebalancing your portfolio (resetting investment percentages back to your original targets) serves multiple purposes:

We monitor your portfolio’s allocations throughout the year and periodically rebalance on your behalf. We believe this transforms market volatility from a concern into a potential advantage. (Click here for more on the benefits of rebalancing.)

Stay Invested: Timing the Market Rarely Works

Even sophisticated investors can be tempted to move in and out of markets based on momentum or emotion. However, research consistently shows how difficult this is to do successfully. Missing just the five best market days between 1980 and 2023 would have significantly reduced a portfolio’s long-term performance.

The most successful wealth strategies keep you invested in the market through full cycles rather than attempt to avoid declines. This is particularly important since many of the market’s strongest days occur during periods of increased downside volatility.

Strategic Opportunities During Market Downturns

Market volatility creates several strategic opportunities:

Your Mindset: Your Greatest Advantage

Often, the biggest threat to long-term performance isn’t market volatility itself but our reactions to that volatility. Here’s how you can stay on track:

The Long-Term Perspective

When viewed over decades, even significant market events—from the 1987 crash to the 2008 financial crisis to the pandemic sell-off—appear as temporary interruptions in a larger wealth-building journey. The data is clear: Markets have historically rewarded patient, disciplined investors.

Maintaining this perspective—especially when headlines suggest otherwise—is often what separates those who simply preserve wealth from those who grow it over time.

Much like a well-constructed March Madness bracket requires looking beyond individual biases to pick the teams that will go the distance, successful investing means not letting short-term market volatility derail your long-term strategy. By understanding market patterns, diversifying wisely, rebalancing regularly and maintaining discipline, you can confidently navigate the madness of the markets without letting temporary declines bust your long-term financial bracket.

Our Latest Videos

This month, Chief Investment Officer Joseph Powers discusses how markets have turned away from the Magnificent Seven and U.S. stocks three months into 2025 and where he’s seeing opportunity.

Click here to watch now.

In addition, Steve Reder, head of wealth management, shares three easy strategies to pass your values to your heirs along with financial assets.

Watch now for his advice.

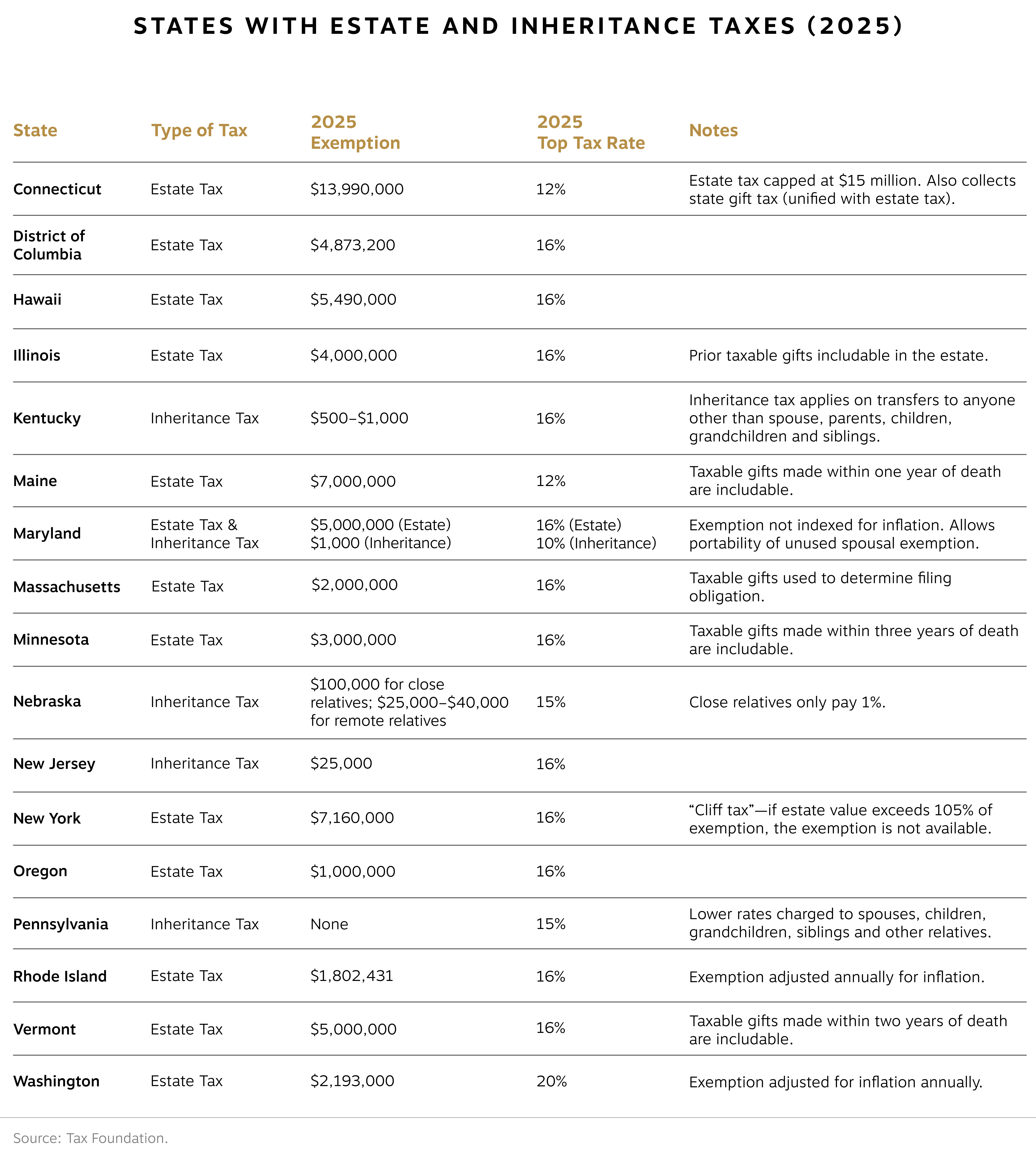

State-level estate and inheritance taxes often have lower exemption thresholds that catch you by surprise. Home equity, life insurance policies in your name and taxable portfolio assets can add up fast. This could significantly reduce what your heirs receive, even if your estate falls well below federal limits. As of tax-year 2025, 16 states and the District of Columbia have estate or inheritance taxes (see table below).

Understanding the Difference: Estate vs. Inheritance Taxes

Estate tax is levied on the deceased’s estate before assets are distributed. The estate itself pays the tax. This is imposed by the federal government and some states.

Inheritance tax is paid by the beneficiaries who receive the inheritance. Certain family members are often exempt or pay reduced rates. There is no federal inheritance tax.

Why State Estate and Inheritance Taxes Matter

These state-level taxes can have a significant impact for several reasons:

While the federal exemption is $13.99 million in 2025 (double that for married couples), individual state exemptions can be as low as $1 million. Note that unlike with federal taxes, a deceased spouse’s exemption does not transfer to the surviving spouse (known as portability) at the state level.

Owning property in a state that imposes these taxes can trigger liability even if you reside in an estate-tax-free state.

In states like Maryland, both estate and inheritance taxes may apply.

According to the Tax Policy Center, state and local governments collected $6.7 billion from these taxes in 2021, making them a sizable revenue source for the states that have them. In other words, states that charge them have a financial incentive to continue doing so.

How To Plan Strategically

Your state of domicile, or where you have your permanent home, determines which state’s estate tax laws apply. Moving to a state without these taxes can yield significant savings.

Key actions to establish domicile include:

States losing wealthy residents may aggressively audit domicile claims, so make sure your documents are in order to avoid complications down the road.

Beware of “clawback” provisions in states like New York, Maine and Minnesota, which can add back recent gifts to your taxable estate.

For married couples, special planning is important. At the federal level, if one spouse doesn’t use their full exemption, the surviving spouse can use what’s left (this is called portability). However, most states don’t allow this sharing between spouses—only Hawaii and Maryland do. For this reason, it can be a good idea to review how your assets as a married couple are titled and potentially transfer assets from one spouse to another to ensure the state estate tax exemption is utilized.

Some couples employ special trusts (called credit shelter trusts) to ensure both spouses fully use their state exemptions. Under current tax law, any money left inside the credit shelter trust after the second spouse’s passing will not be subject to estate taxes, so the goal is typically to leave it untouched for as long as possible. Some states also allow special arrangements (called QTIP elections) that can help married couples minimize both federal and state taxes.

When properly structured through an irrevocable life insurance trust (ILIT), life insurance proceeds can provide a source of funds to pay estate taxes without adding to the taxable estate.

This strategy is particularly valuable for:

Be Prepared

While federal estate tax affects relatively few Americans, state estate and inheritance taxes impact many more families with moderate wealth. With exemptions as low as $1 million in some states, even homeowners in high-value markets may face significant exposure based on the assessed value of their home.

If you live in or own property in a state that charges estate or inheritance taxes (or are considering moving to one), talk to your team so we can help you to consider this additional tax liability in your plan.