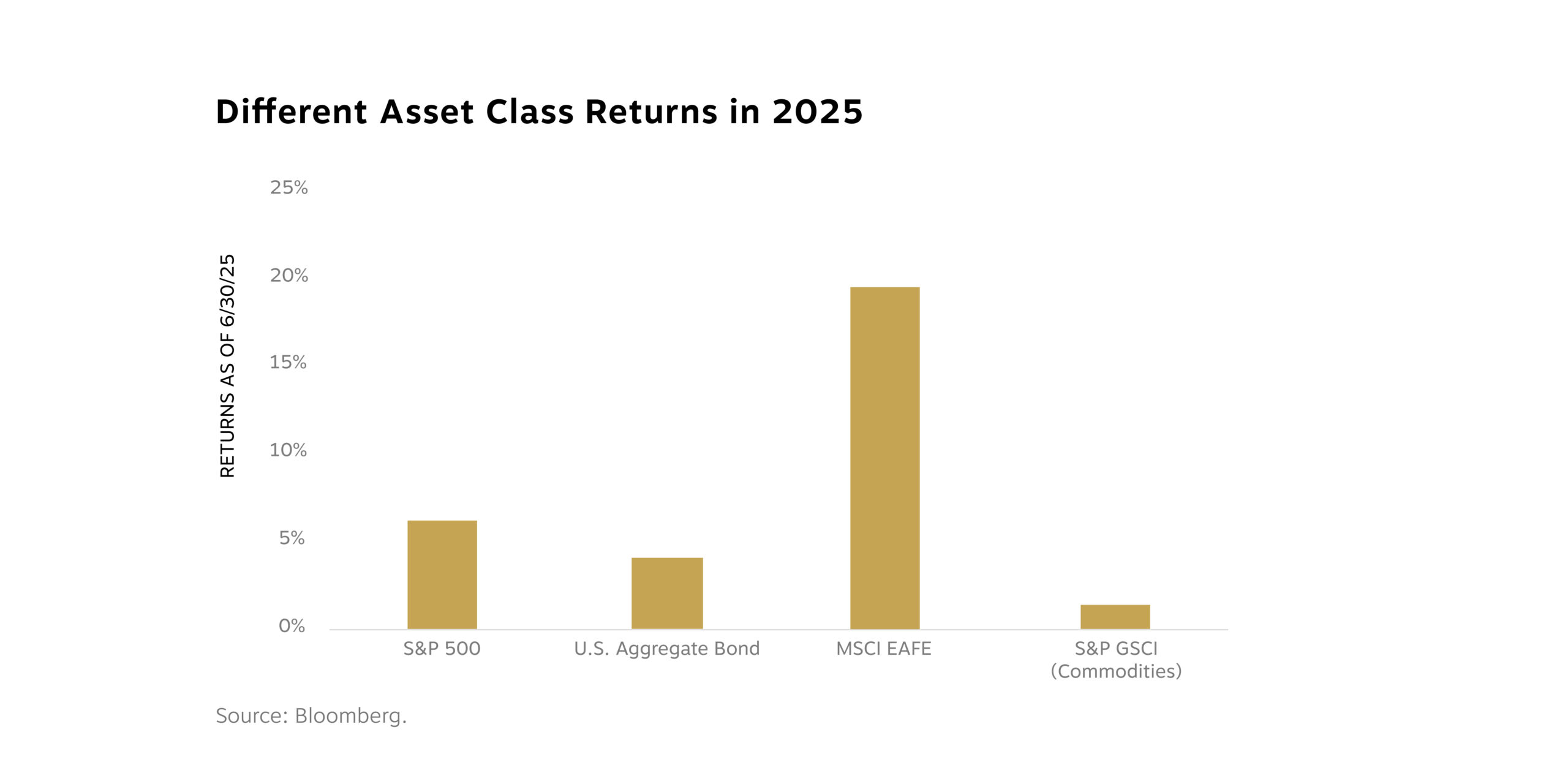

It’s been a welcome turnaround for investors. Just a few months ago, markets were down 20% in a matter of weeks as stalling trade talks and the potential disruption to AI infrastructure from DeepSeek rattled traders. But many of those concerns have been replaced with renewed optimism even as the tariff and AI stories continue to develop. Stocks have rallied in response, rewarding investors who stayed disciplined and focused on long-term outcomes. At the end of June, the S&P 500 index was up 6.2% year to date.

Bonds have been a stabilizing influence for diversified investors, returning 4.0% in 2025 through the second quarter. After a volatile stretch, longer-term yields have drifted lower as inflation hovers around 2.5% and the market grows more confident that the Federal Reserve may start cutting rates later this quarter.

Foreign stocks have been a highlight—particularly in developed economies. The MSCI EAFE index has more than tripled the return of U.S. stocks year to date with a 19.4% first-half gain. Valuations remain compelling, and economic momentum abroad is beginning to firm up.

On the other end of the spectrum, commodities have had lackluster results, gaining just 3.3% through Q2. While there was concern that new tariffs would cause rapid inflation and that conflict in the Middle East would cause the price of oil to spike, that hasn’t materialized in any meaningful way, yet. As a result, this area of the market remains under pressure.

Reasons for Market Resilience

So what’s driving this confidence in equities? In short, the health of the consumer. President Trump’s administration continues to dominate headlines, but behind the noise, we’ve seen resilience in the job market and inflation trending in the right direction over the last three years.

Unemployment declined to 4.1% in June, labor participation is steady and wage growth is cooling—but still positive. This dynamic supports consumer activity without fueling inflation. As goes the consumer, so typically goes the economy—when people have steady jobs, they tend to spend, creating a virtuous cycle for growth.

Inflation has stubbornly held above the Fed’s 2.0% target, but it’s been trending in the right direction for most of 2025. That said, some cracks may be forming. After months of gradual moves lower, June’s consumer price index showed headline inflation running at 2.7%, the highest in four months. Excluding food and energy prices, inflation showed a 2.9% annual pace. Driving the uptick were prices for goods that are more sensitive to a rise in tariffs—furniture, apparel, toys and appliances. These price increases accelerated at the end of the second quarter. This indicates at least some businesses are now passing on cost increases to the consumer, though one month does not a trend make.

For now, the combination of moderating inflation and strong employment has been a driving force behind stock market gains. We’ve worked to position your portfolios to participate when markets are rising and provide defense if they reverse course, and diversification is a key aspect of that discipline.

The Fiscal Outlook Caveat

That said, a longer-term theme may work against the economy: the fiscal outlook.

The nearly 900-page One Big Beautiful Bill Act signed into law on July 4 includes many new provisions but was centered around making permanent the cuts in the Tax Cuts and Jobs Act of 2017. (For more on what’s included and how you can benefit, please scroll down to the next story, What the One Big Beautiful Bill Means for You, Your Family and Your Wealth.)

While many of these tax policies are not entirely new, extending them avoids a jump in tax liability for higher earners that would have occurred had the policies expired as scheduled at the end of 2025. The law also includes significant cuts to social safety net programs and increases the budget to carry out Trump’s immigration agenda. Despite slashing spending in some areas, extending the tax cuts raises cost concerns for the U.S. budget.

The Congressional Budget Office estimates this law will add about $3.3 trillion to the federal deficit over the next decade. Some of that may be offset by additional growth or tariff revenues, but credit rating agencies have taken note, and we’re already seeing pressure on the long end of the Treasury curve as a result, pushing prices lower and yields higher.

Looking Ahead

With a dizzying array of narratives and market twists and turns already behind us, here are some of the key themes to watch over the second half of the year.

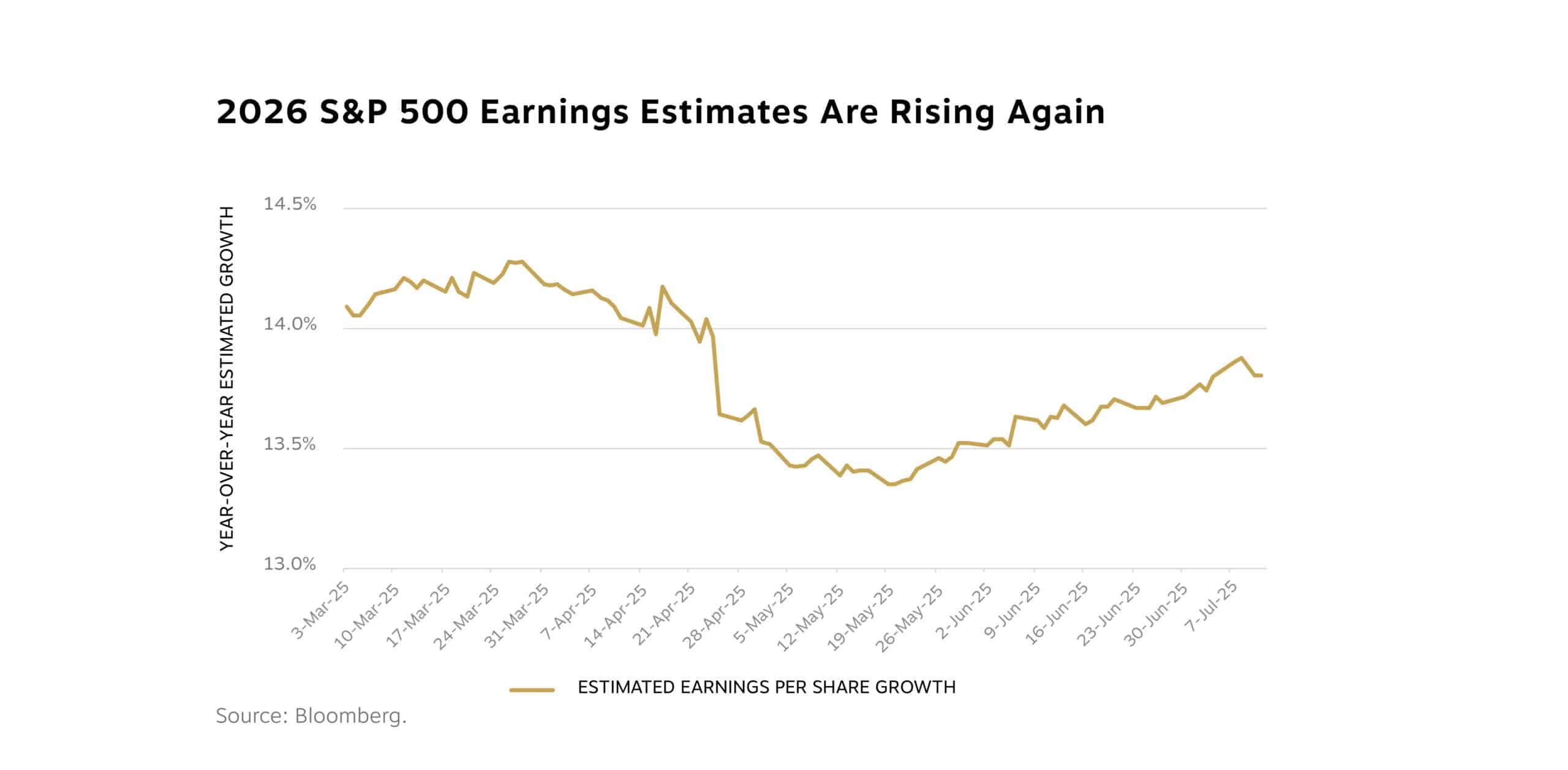

First, corporate earnings expectations have improved. Tariff concerns have been dialed back, and companies are adjusting as we expected they would, particularly larger companies with the resources and reach to do so. Analysts now project nearly 10% earnings growth for 2025, up from mid-single digits just a few months ago. That’s been a key driver of market gains. It’s early in the second-quarter earnings reporting season, but if current results hold, Q2 will mark eight consecutive quarters of year-over-year earnings growth for S&P 500 companies. And as you can see in this chart, expectations for growth are even better in 2026.

Second, the Federal Reserve is likely to adjust policy soon. While a July cut seems unlikely, we expect Chair Powell may use his Jackson Hole speech next month to signal a potential September move—assuming inflation does not creep any higher and economic growth remains steady. For now, the opportunity to benefit from higher rates on bonds remains intact. At current yields, investment-grade options across both corporate and municipal bonds offer compelling returns and can provide meaningful income and stability in a portfolio.

Finally, valuations could still present opportunity, particularly outside the U.S., as developed foreign markets remain attractively valued, with room for multiple expansion as fundamentals improve.

We believe we’re well positioned to face what comes, and we’re mindful of potential risks to the equity and bond markets. If you have any questions about your portfolio or plan, please contact your team.

Our Latest Videos & Media Appearances

Chief Investment Officer Joseph “JP” Powers recaps recent market and economic trends and discusses the themes he’s watching in the second half of 2025. Click here to watch now!

Diana Linn, partner and wealth advisor, shares her perspective on how we approach the financial aspects of divorce with clients. In a stressful time, having a trusted partner to answer questions and guide you through important decisions can provide welcome relief. Hear what Diana has to say.

CEO Michelle Knight was recently featured in Barron’s Advisor, where she talks about how she came to the financial industry, her perspective on leadership, the future for RWA and more. Read it here.