The AI and mega-cap stock story has dominated the narrative for investors once again this year. Narrow participation and high valuations for these stocks could be a liability if earnings results disappoint. We also continue to deal with policy uncertainty out of Washington and geopolitical tensions abroad, though the ceasefire between Israel and Palestine was welcome news.

On the positive side of the ledger, markets are pricing in multiple Federal Reserve rate cuts, which provides some support to stocks and other riskier assets. We’ve also seen continued economic growth and inflation that’s meandering around 3.0% (still above target), which could help both stocks and bonds. Returns have broadened to include more participation from small caps, but big tech and communications stocks are the undisputed leaders this year once again. As we explore below, foreign stocks have been a positive for diversified investors and are on track to outperform U.S. stocks in a calendar year for the first time since 2022 (when they declined less—2017 was the last year in which foreign stocks outperformed U.S. stocks to the upside).

The absence of timely economic data due to the government shutdown could be problematic if it’s sustained, but time and again, investors have shrugged off negativity and driven markets higher. And the economic impacts of shutdowns are typically quickly recovered once the government reopens.

We’re here to manage through distractions, uncertainty and anxiety and make sure that specters conjured by headlines or the latest outrage do not chase you off course. For now, we see opportunities to take advantage of market strength by rebalancing and refilling your liquidity coffers, and we’re looking ahead to furthering your goals in 2026 and beyond.

Markets Recap

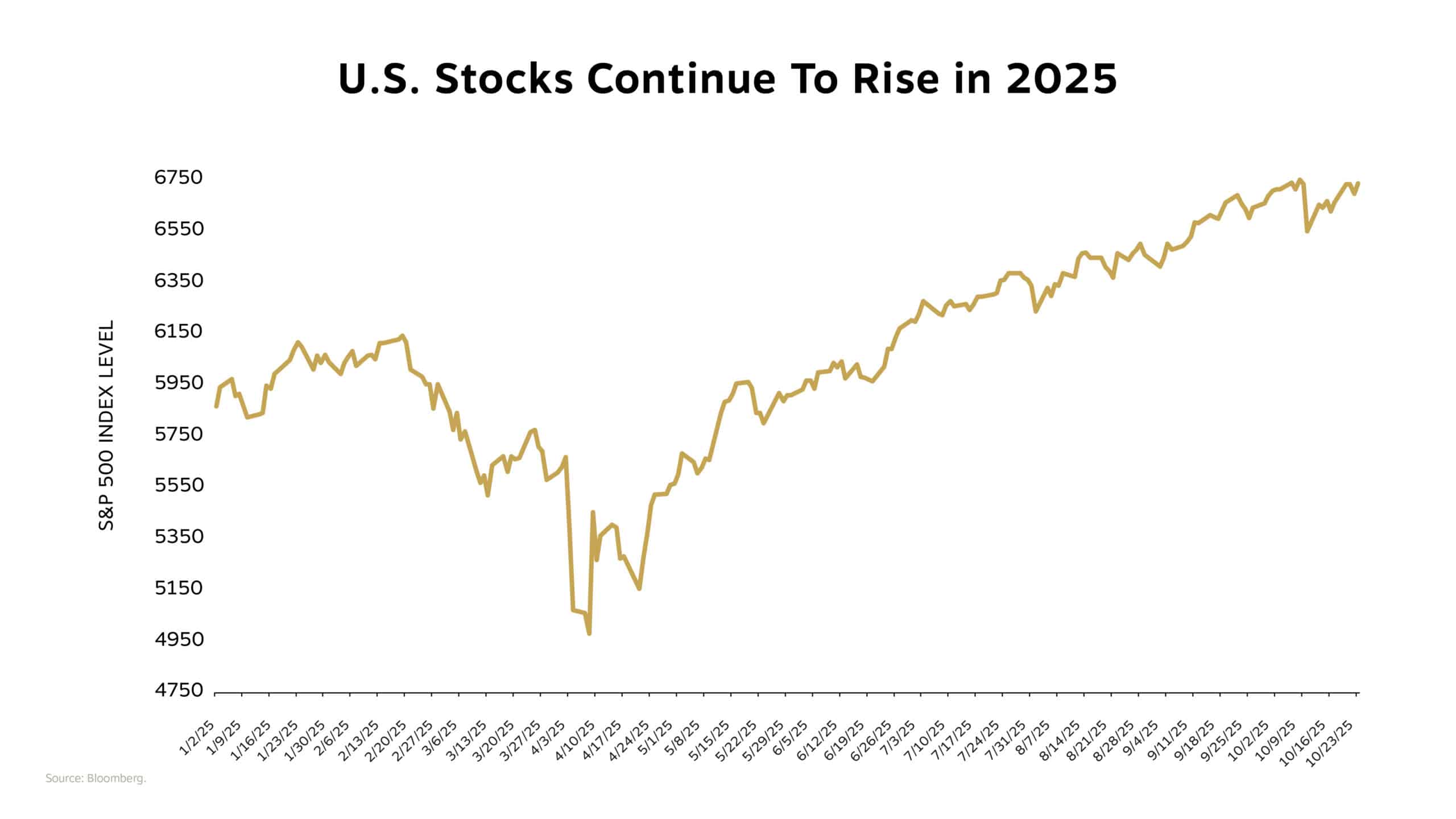

The S&P 500 has extended this year’s gains despite some bumpiness earlier this month when President Trump floated a renewed tariff fight with China. As with other tariff threats and posturing, the impact on markets quickly passed, and they resumed their climb higher.

Since the government shutdown has delayed the release of key economic data that would typically be impacting markets, earnings season has taken center stage as we look ahead—and so far, results have been surprisingly strong.

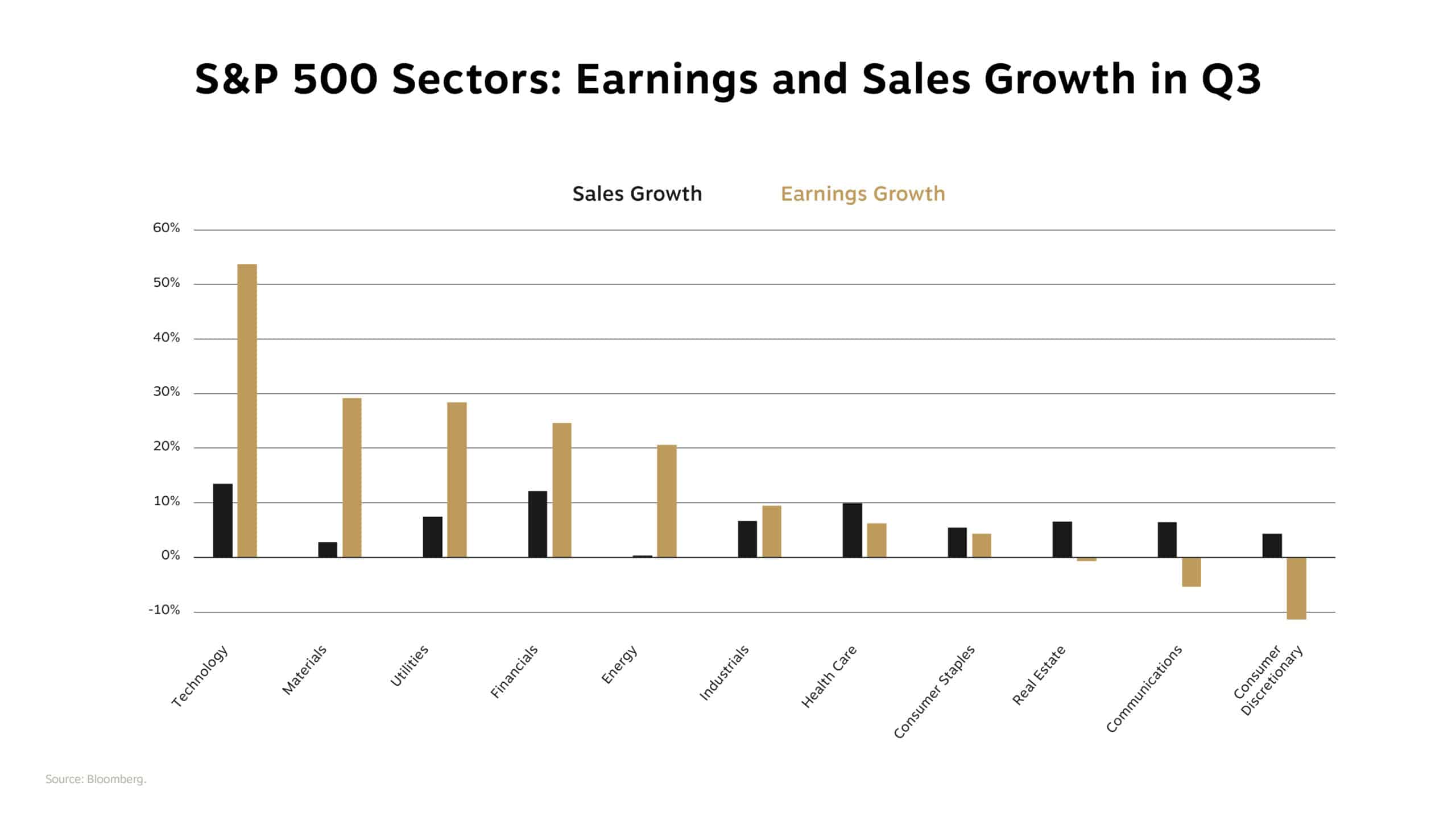

While it’s still early, with only about a quarter of companies in the S&P 500 reporting, sales growth is running at almost 8% and earnings are up over 15%.

And at the sector level, technology, industrial and financial stocks have delivered some particularly bright results, with strong margins and better-than-expected guidance. Utilities have also shown significant earnings growth, and we’ll get into the why momentarily. But outside those sectors, performance has been more mixed.

Communications and consumer discretionary sectors have shown strength recently, but there are signs of pressure from rising costs and some slowing demand. It’s still early in the earnings season, and key companies like Meta, Google and Nvidia are among the major names whose results will likely influence market direction.

The Fed, Rates, Gold and Global Leadership

The Federal Reserve met this week, and as we’ve written before, the central bank faces a delicate balancing act. Progress lowering inflation has slowed, fiscal deficits remain large and political pressure on rate policy is mounting.

With all that, as expected, the Fed cut rates by another 25 basis points, despite equity markets making new highs. While the Fed didn’t want to wait for an economic slowdown to start cutting rates, this highlights the clear mismatch between returns in the market and what the Fed is seeing in its economic outlook.

Still, it’s worth pointing out that, alongside the U.K., we have the highest level of rates of the major central banks, so there is room to cut and find an equilibrium rate probably somewhere in the mid to high 3% range early next year. From there, the Fed can be more data dependent—assuming the government is open and releasing economic data by then.

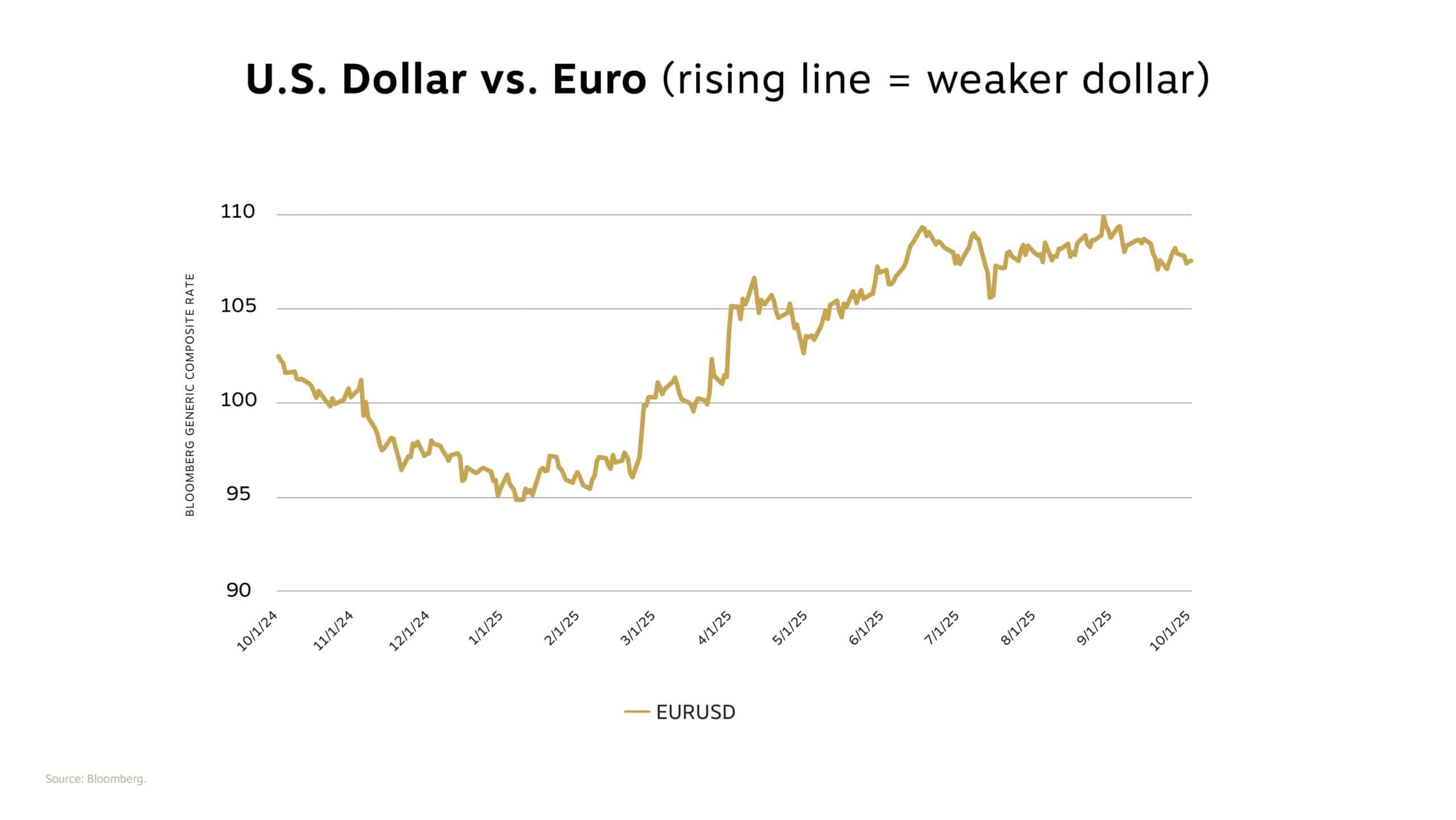

So, with interest rates on the decline, the national debt expanding, and both trade and immigration policies in flux, you can see why the dollar has been under downward pressure this year—highlighted by a comparison of the dollar against the euro over the last 12 months.

These factors have not just impacted the value of the dollar but have contributed to assets like gold surging to all-time highs. Several dynamics are at play, including central banks buying gold as they look to diversify away from the dollar, but much of this development stems from retail investors piling in through ETFs.

But the bigger story may be overseas. The perception of waning U.S. leadership has triggered a significant rally in foreign equity markets. While the S&P 500 is up about 14% this year, countries like Germany are up nearly 40%, China is up roughly 30% and the seldom quoted IBEX 35 index, which represents Spain’s largest stocks, is up over 50%.

Cheaper valuations, earlier rate cuts abroad and currency strength have made 2025 one of the strongest years for international outperformance in over a decade. When confidence in the dollar softens, global capital tends to rotate—and we’re seeing that shift play out in real time.

The AI Energy Story

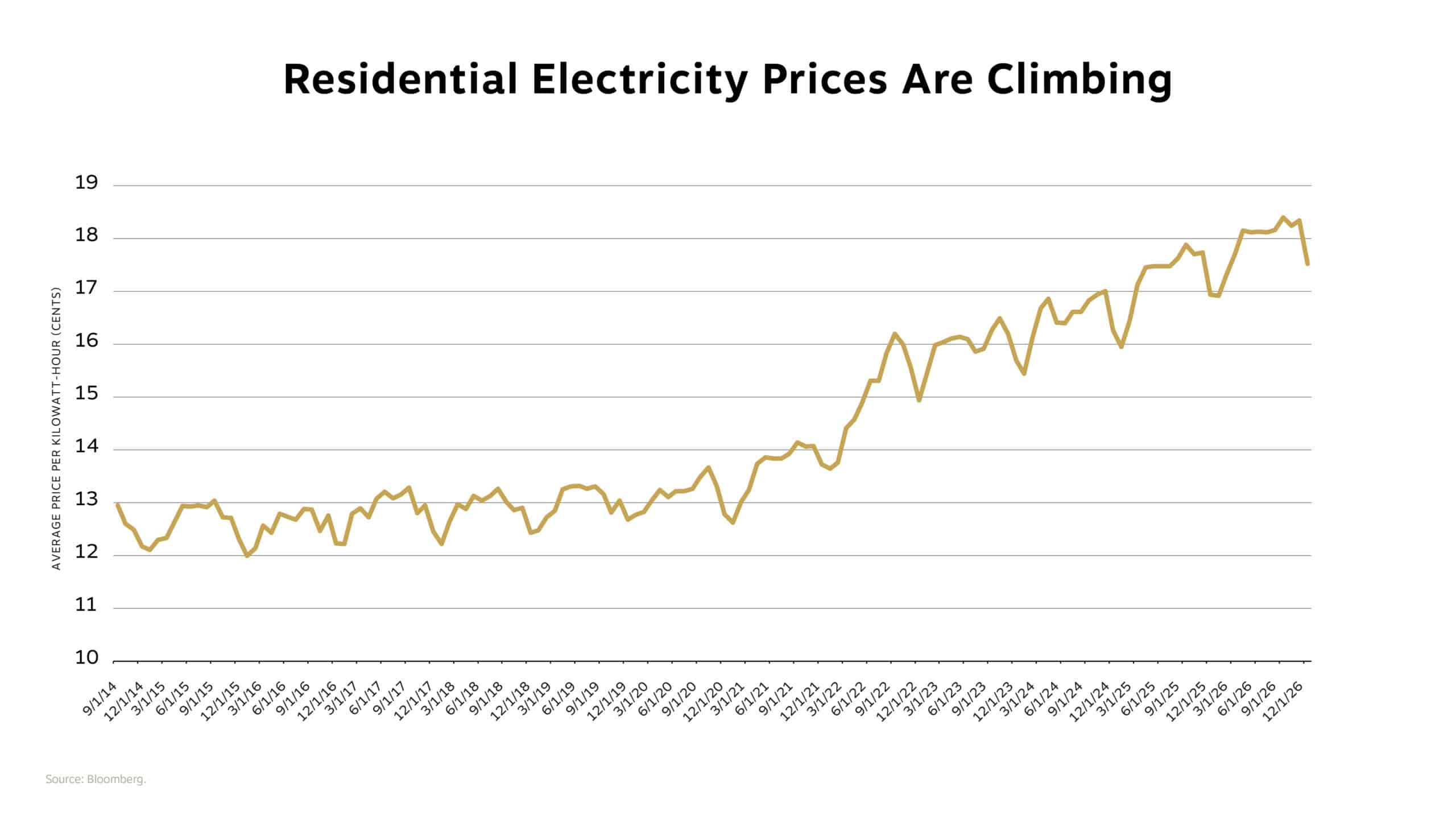

As more users begin to incorporate AI tools into their work and home lives on a regular basis, the data centers powering the models behind these tools are consuming increasingly large amounts of electricity. According to recent projections, global power demand from data centers is expected to double in the next few years.

Utility companies are scrambling to meet that demand, and you may have noticed a shift in your own energy bills as a result. The price of residential electricity has been on the rise the last few years as the cost of meeting data centers’ electricity use gets passed on to consumers.

So, while oil and gas prices have eased, the savings at the pump have been offset by an increase in your electric bill. And it’s not likely to slow any time soon as the demand for electricity continues to ramp up.

From an investment standpoint, when we think about the opportunities that this could create, we look beyond traditional energy or commodity investments. The benchmark Goldman Sachs Commodity Index (GSCI) has had an up-and-down run but has done little for investors seeking to track its performance. That’s because the bulk of the index is tied to oil and not to electricity generation.

The price of West Texas crude oil has actually come down materially over the last year as demand for other sources of energy has picked up. This surge in electricity demand is reviving interest in nuclear power. And uranium prices have caught the attention of investors.

The winners are at the company level instead of in the commodities or utilities themselves. Companies like Oklo, a nuclear power operator, and Cameco, which makes uranium, have seen their stocks appreciate rapidly in this environment—far outpacing the results of the commodities in this space.

For energy investors across the globe, this marks a shift—from oil barrels to electrons—as AI reshapes not just productivity but power consumption itself.

Looking Ahead

So, where does all that leave us? Economic and consumer resilience continues to win over the equity markets, gold’s rally signals waning confidence in the dollar and perhaps the U.S. as a whole, and international markets are taking leadership for the first time in years. And while AI is transforming technology, it’s also rewriting the global energy story.

While we do not believe markets are hunting ghosts—they’re instead on the trail of real economic and equity phenomena—we’re aware of just how thin the line can be between sentiment and facts that move markets. Our investment team, portfolio managers, financial planners and tax professionals are continually monitoring for areas of risk and opportunity for your portfolio and wealth plan. Meanwhile, our advisors, client officers and client service team members are working hard to hold monsters real and imagined at bay to help safeguard your accounts. Happy Halloween!

Our Latest Videos, Media Mentions & Our New Podcast

Chief Investment Officer Joseph “JP” Powers discusses the themes we’re tracking as the fourth quarter progresses. Click here to watch now!

Associate Portfolio Manager Josh Jurbala reviews how private equity, private credit and real assets can broaden investment opportunities beyond the public markets. Watch now.

Head of Family Office Fiduciary Services Jacqueline Rahn shares what to consider when choosing a trustee and why selecting the right person can make all the difference. Watch now.

This month, we’re thrilled to launch The Human Side of Wealth Podcast. In our debut episode, Andrew Busa, director of financial planning, and Steve Reder, president of Private Wealth, dive into the emotional side of money. From childhood memories to legacy planning, they share real client stories and personal reflections that reveal how financial decisions are deeply tied to values and relationships. Listen now!

RWA was honored to earn the #20 spot on Forbes’ Top RIA Firms list for 2025. This list ranks 250 independent advisory firms by qualitative and quantitative data, including revenue trends, assets under management, compliance records and industry experience.

The Forbes 2025 Top RIA Firms list includes 250 independent advisory firms with cumulative assets of more than $1.9 trillion. The ranking was developed by SHOOK Research and is based on an algorithm of qualitative criteria, mostly gained through telephone, virtual and in-person due diligence interviews and quantitative data as of 3/31/25. The algorithm weighs factors like revenue trends, assets under management, compliance records, industry experience, and those that encompass best practices and approaches to working with clients. Firms were required to submit a formal survey. There was no fee associated with participation. View the list ranking methodology.