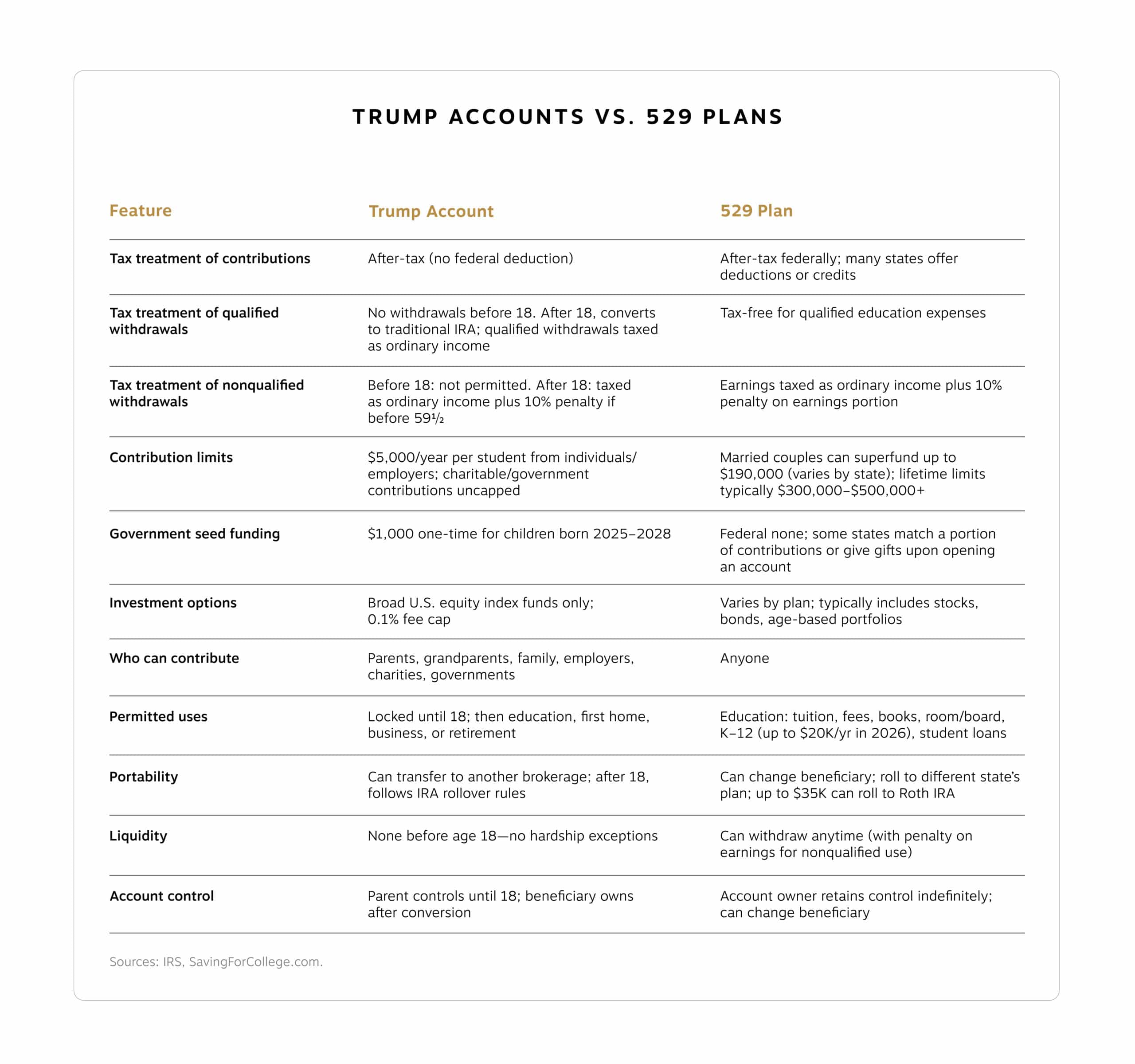

What Are Trump Accounts?

In short: tax-advantaged investment accounts designed for children under 18. Think of them as a hybrid between a traditional IRA and a 529 college savings plan—with some important distinctions.

The accounts will become available for contributions on July 4, 2026 (America’s 250th anniversary). Parents, grandparents and employers can contribute up to $5,000 per year per child. Charitable organizations can also make contributions without limit. The funds must invest in broad U.S. equity index funds like the S&P 500. And fees are capped at just 0.1% annually.

The Government’s Gift

Perhaps the most notable feature is the $1,000 government contribution available to children born between Jan. 1, 2025, and Dec. 31, 2028. This seed funding requires nothing more than opting in at enrollment, and families of any income level qualify.

The program already has a boost from a private donor. The Michael & Susan Dell Foundation recently pledged $6.25 billion to provide $250 contributions to 25 million children ages 10 and younger in lower-income ZIP codes. Other corporations, including Nvidia and Robinhood, have signaled interest in contributing to employee accounts. Additional charitable and employer contributions in the years ahead are a distinct possibility.

Trump Account Trade-Offs

Trump Accounts come with meaningful restrictions. The money is inaccessible until the child turns 18. There are no exceptions for financial hardship, pre-college education expenses or emergencies. The accounts must also invest in funds focused on U.S. companies’ stocks, limiting the opportunity to diversify risks and assets. This is a significant departure from 529 plans, which allow qualified education withdrawals at any time (though only up to $20,000 per year for private K–12 tuition) and include a wide range of global stock, bond and money market funds as investment options.

Once the child reaches 18, the account converts to a traditional IRA. Withdrawals before age 59 ½ for nonqualified purposes will trigger ordinary income tax plus a 10% penalty. Qualified purposes include higher education, purchasing a first home or starting a business.

Parents or contributors must fill out a tax form (the not-yet-available “Form 4547”) to establish the account, opt in to the seed money and make investments. This process is more cumbersome than establishing a 529 plan account or IRA.

You’ll also need to be aware of that $5,000 limit. Let’s say your employer makes a $1,000 contribution for your child and then a grandparent separately contributes $5,000. That would put the account $1,000 above its annual limit, and the excess contributions would have to be withdrawn or potentially incur a 6% annual penalty (the same as for traditional IRAs). Other Education Savings Vehicles

Other Education Savings Vehicles

Trump Accounts and 529 plans aren’t the only choices. Depending on your goals, you have other options to consider:

Coverdell Education Savings Accounts (ESAs) offer tax-free growth for education expenses with more investment flexibility than 529s, though contributions are limited to $2,000 annually and phase out at higher incomes.

Custodial accounts (UTMA/UGMA) provide maximum flexibility—funds can be used for any purpose—but the child gains full control at the age of majority (18 or 21, depending on the state), and there’s no special tax advantage.

Roth IRAs for children are an option if your child has earned income. Contributions grow tax-free, and withdrawals in retirement are tax-free as well. Qualified education expenses do not trigger the early withdrawal penalty, but earnings on contributions are subject to income tax.

Crummey trusts allow you to transfer assets to a child or grandchild while qualifying for the annual gift tax exclusion. There are no restrictions on how the funds are used, but withdrawals do not receive special tax treatment for education expenses.

Our Opinion

Because of the tax treatment and other restrictions, we believe the greatest value of these accounts is the $1,000 government gift for children born between Jan. 1 this year and Dec. 31, 2028. Any future charitable gifts by third-party organizations will be a bonus. Most investors will have other education savings and wealth transfer strategies available to them that come with fewer strings attached.

If education funding is your priority, a 529 plan likely remains the more flexible and tax-efficient choice, and it allows you to save significantly more per year for each beneficiary. If you’re already maximizing other tax-advantaged accounts and want another avenue for long-term wealth transfer, Trump Accounts could play a supporting role in your strategy, but the options shared above may better serve the same purpose. We believe it’s in your best interest to explore the choices accessible to you before investing your own money in a Trump Account.

Your RWA team is happy to work with you to understand how these new accounts might fit into your overall plan.

Our Latest Video

In his December market update, CIO Joseph “JP” Powers unpacks the latest economic data following the government reopening, reviews what worked and what didn’t in 2025, and outlines key priorities for the year ahead. Watch now!

Community

Giving back and helping provide for future generations is a treasured part of our lives at RWA. These are a few of the most memorable events this year.

In May, our Family Office team was proud to represent the firm at the 21st annual Party in the Park, supporting the Emerald Necklace Conservancy and Boston’s iconic park system. We’re grateful to play a small part in a mission that nurtures nature and community.

This fall, we donated securely wiped and refurbished laptops to South Boston Neighborhood House. Once used to help grow our business, these computers will now support growth opportunities for seniors, families and students in our community.

Most recently, we hosted students from Cathedral High School in our Newton office to help them explore careers in the financial services and wealth management industry. They asked smart questions and brought fantastic energy to the gathering.

Thoughts and Expertise

The contributions from our talented team members, who stepped forward to share guidance with you in print, on video and through the debut of The Human Side of Wealth podcast, made 2025 a memorable year for RWA. Here’s what you may have missed or wish to revisit ahead of the new year.

Perhaps the biggest news for investors and taxpayers alike was the passage of the One Big Beautiful Bill Act, which brought sweeping changes to tax law. This article outlines how the act could impact you.

If you’d rather watch than read, our video series has you covered. This is just a sampling of what we’ve shared over the last 12 months:

- President of Private Wealth Steve Reder shares three strategies for passing on more than money to the next generation.

- Jacqueline Rahn, head of Family Office fiduciary services, discusses the importance of selecting the right trustee to protect your legacy and support your loved ones.

- Portfolio Manager Jennifer Loveless reviews practical steps to help you and your family get organized, reduce risk and put cash to work.

- Josh Jurbala, associate portfolio manager, alternatives, looks at how private equity, private credit and real assets can broaden investment opportunities beyond the public markets.

After launching The Human Side of Wealth podcast this fall, we’ve produced three episodes, with more to come. You can find them here:

- “Why Money Is More Than Math.” In our debut episode, Director of Private Wealth Financial Planning Andrew Busa (our host) and President of Private Wealth Steve Reder explore how values, relationships and life experiences shape financial decisions and why true wealth starts with understanding your “why.”

- “What the New Tax Law Means for You.” Host Andrew Busa and Tax Associate Christopher Hernandez unpack the biggest tax changes in years and discuss what they mean for families, business owners and retirees.

- “Charitable Giving Strategies That Go Beyond the Numbers.” In this episode, Andrew is joined by President of Family Office Nicole LaChappelle and Steve Reder to unpack the art and science of charitable giving, covering smart strategies, family conversations and legacy planning.

Recognition

Beyond the above, 2025 was a humbling and gratifying year for RWA, as we enjoyed coverage in prominent publications nationwide, including Barron’s, Forbes, the Boston Business Journal and InvestmentNews.

In June, Barron’s Advisor interviewed CEO and Chief Economist Michelle Knight. The conversation touched on Michelle’s career path, her thoughts on the economy (at the time—you can find her latest thinking each week here), her philosophy on helping clients manage their wealth and more.

We owe you a debt of gratitude for putting us in a position to be seen, to be heard and to make an impact, and we’re looking forward to what we can achieve together in 2026. Thank you for a great year!