The Test of Discipline

From 2010 through 2024, U.S. stocks delivered total returns exceeding 600% compared with less than 100% for international markets. Year after year, investors wondered: “Why do we still own international stocks when U.S. markets keep winning?”

It’s a fair question. Watching one part of your portfolio consistently lag the other requires conviction. Some investors abandoned international exposure entirely, betting that U.S. tech giants would continue their dominance indefinitely. The temptation to chase recent winners is always powerful.

But as wealth managers, we know that market cycles don’t last forever. History shows us that leadership rotates between regions—U.S. stocks led in the 1990s and 2010s, while international markets had their turn in the 1980s and 2000s. More recently, foreign stocks outperformed U.S. markets in 2017 and 2022. Our job is to position portfolios for the full cycle, not just the most recent chapter.

When the Cycle Turns

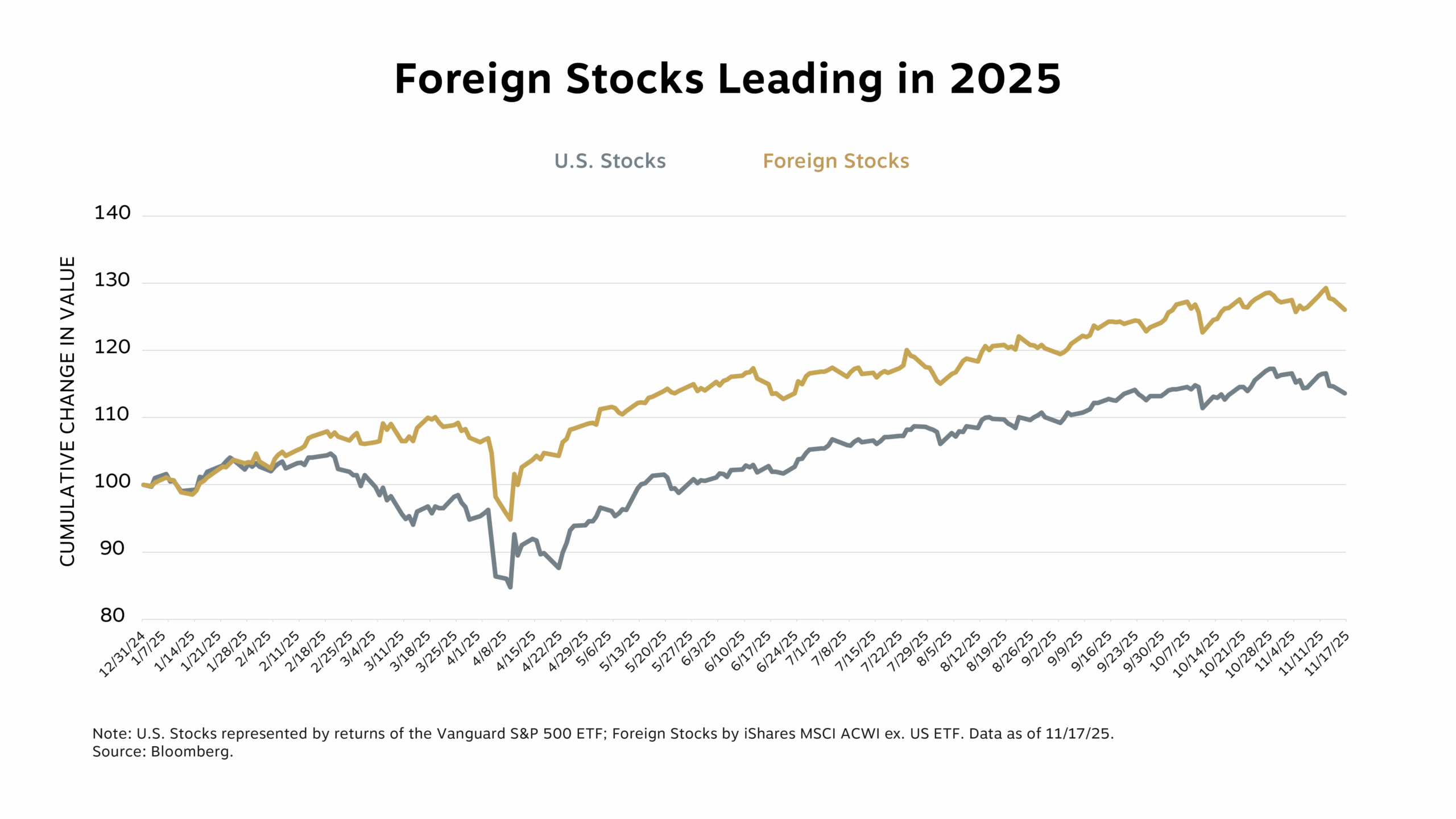

This April brought a stark illustration of why diversification matters. When President Trump announced sweeping tariffs on April 2—what he called “Liberation Day”—U.S. markets reacted sharply. The S&P 500 dropped 15% from its peak, with the decline happening in just days.

International markets, while not immune to the shock, proved more resilient. They experienced less volatility and recovered faster. Though U.S. markets rebounded to reach new highs by late June (and have since made new records), the turbulence demonstrated the real-world value of geographic diversification. This wasn’t luck—it was the natural result of different markets having different exposures to U.S. policy uncertainty.

By maintaining international exposure, diversified portfolios absorbed the turbulence better. They also participated fully in the international surge that followed, as global investors reconsidered their heavy U.S. concentration.

Today’s Opportunity

International markets aren’t just rewarding past patience—they’re presenting compelling opportunities going forward.

The valuation gap has widened dramatically. International stocks trade at roughly 13 to 14 times forward earnings compared with 21 times for the S&P 500. That represents about a 35% discount for similar-quality companies, simply based on where they’re headquartered.

Concentration is another factor. The five largest U.S. companies—Apple, Microsoft, Nvidia, Amazon and Alphabet—now represent more than a quarter of the S&P 500’s value. In international markets, the top five holdings account for just 7% of the index. This diversification within diversification provides additional portfolio resilience.

The weakening dollar has amplified international returns for U.S. investors. When foreign currencies strengthen against the dollar, as they have this year with an 8% decline in the dollar index, international investments are worth more when converted back to dollars.

Our Commitment to Diversification

As your wealth managers, we embrace diversification because we’re focused on the long term. We aim to be nimble in adjusting to changing conditions, but not reactionary to short-term performance.

Would it have been easier to abandon international stocks after years of underperformance? Certainly. Would it have felt satisfying in 2023 when U.S. tech stocks soared? Absolutely.

But market timing—whether between asset classes or geographic regions—has proved to be a losing strategy over time. The best performers often come from unexpected places at unexpected times. By the time outperformance becomes obvious to everyone, much of the opportunity has already passed.

The Season of Giving Back

This November, as we reflect on giving back, international stocks are doing exactly that for investors who stayed diversified. The patience required to maintain global exposure through the U.S. winning streak is now being rewarded with stronger returns and smoother volatility.

More importantly, this moment reinforces a fundamental principle: Diversification works not because every holding wins every year, but because different investments take turns leading. We recommend holding foreign stocks in portfolios precisely for years like 2025.

Market cycles will continue to rotate. U.S. stocks will have their time to lead again. But trying to predict and trade these cycles is far riskier than simply maintaining balanced exposure and letting global opportunities unfold as they will.

That’s the real goal of diversification—not perfect timing, but consistent participation wherever growth happens to emerge within your portfolio.