So far, market reactions have been negative but measured. The broader stock market has pulled back modestly, while some segments and industries directly tied to global energy flows have experienced greater pressure.

In moments like this, perspective helps. Markets tend to react quickly to uncertainty, but the lasting impact depends on whether events translate into real economic disruption like sustained energy shortages, impaired trade routes, a renewed push on inflation or tighter financial conditions. That lens guides our outlook.

Energy Markets Are on the Front Lines

The initial market response followed a familiar pattern: Oil prices moved higher as investors priced in the risk of disruption, inflation expectations ticked up modestly and energy stocks outperformed in the early days.

At this stage, markets appear to be pricing risk and not necessarily lasting supply losses. That distinction matters. If physical supply were meaningfully disrupted, the implications would be more serious. And duration matters: The longer tensions persist and interfere with energy flows, the greater the risk of inflationary pressures and slower growth.

Investors have reacted to the conflict by moving into traditional safe havens such as Treasurys, the dollar and more defensive equity sectors. Historically, these shifts are most pronounced early on. If conflicts do not broaden or disrupt global trade, markets often refocus on economic fundamentals over time. So, these safe-haven flows are best viewed as short‑term risk management and probably not signals that the economy is weakening.

Why Oil’s Path Shapes the Fed Debate

Sustained increases in oil prices can complicate the inflation outlook, which is why energy markets play an outsized role in shaping expectations for Federal Reserve policy. Higher oil prices can influence inflation readings more quickly than many other factors, even when the broader economy remains resilient.

That said, our expectations have not changed. Higher energy costs are a headwind, not a wholesale shift in the story. The key question is whether inflation will continue to move gradually toward target levels. This would give policymakers confidence around the timing of future rate cuts. At its March meeting, the Fed’s governors elected to keep interest rates where they are for now, acknowledging the uncertainty the Middle East situation has introduced to the economic environment.

It’s also worth remembering that our economy today is built differently than it was in prior Middle East crises. We are much less energy‑dependent than in prior decades, benefiting from greater domestic production and supported by generally resilient corporate balance sheets. Earnings growth continues to be driven far more by domestic demand and productivity trends than by direct exposure to the region. Historically, geopolitical shocks that don’t impair global trade or financial systems have tended to produce short‑term volatility followed by stabilization.

Positioning: Balance Over Prediction

We can’t predict headlines. But we can prepare our portfolios for uncertainty. In this environment, our emphasis remains on balance:

- Quality and diversification: Uncertainty often widens the gap between winners and losers. Maintaining diversified exposure and an emphasis on quality can help manage risk without giving up long‑term opportunity.

- Income and ballast: High-quality bonds continue to offer meaningful income and can help cushion portfolios during periods of stock market volatility.

- Real assets and selective alternatives: Think infrastructure, real estate and carefully chosen hedged strategies for added diversification and potential inflation protection, where appropriate.

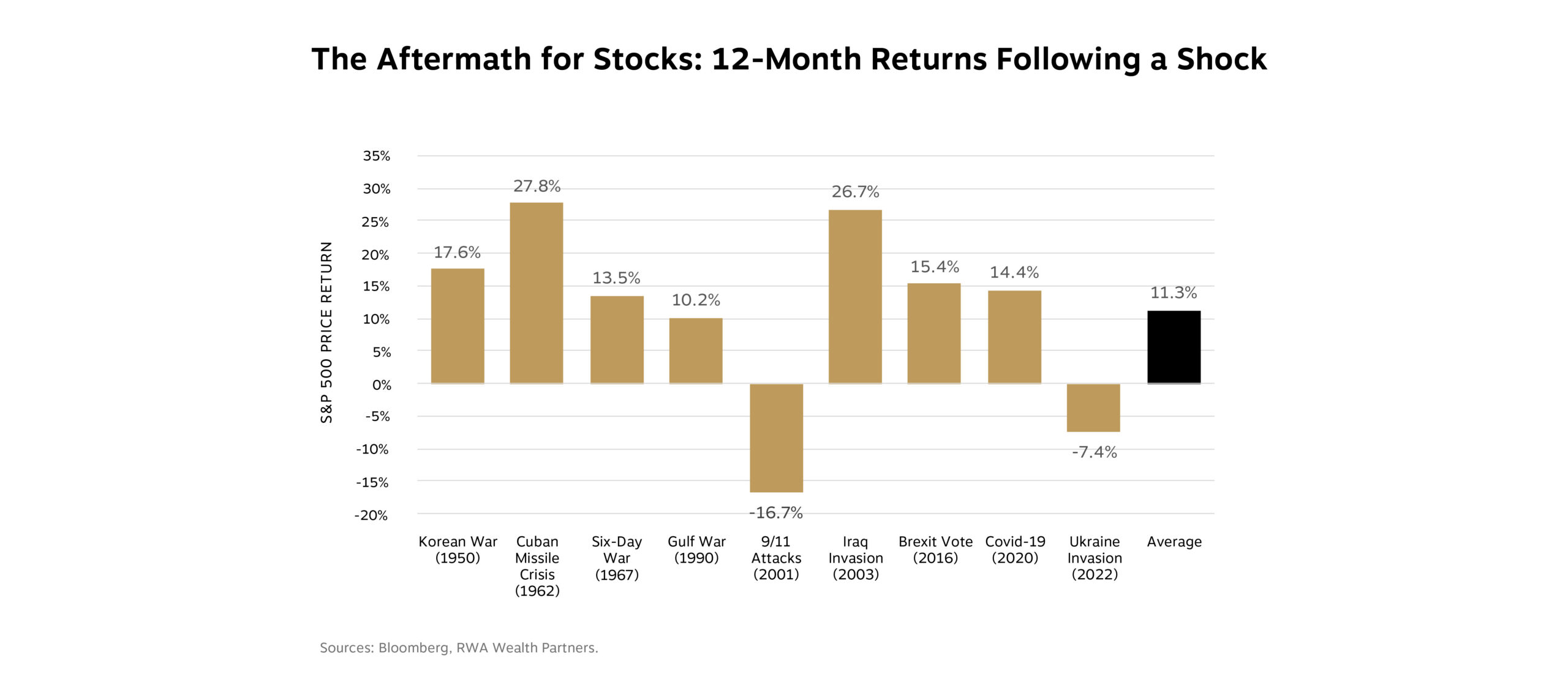

Stocks After Major Geopolitical Events

Outcomes have varied, but history offers an important perspective. In most cases, markets posted positive returns in the year following these events. When outcomes were negative, they typically coincided with broader economic stress rather than the geopolitical event alone.

That pattern reflects what we often see in real time: Markets quickly reprice uncertainty, then return to fundamentals like growth, earnings, policy and liquidity. Even when geopolitical events were unsettling, history shows that many were ultimately manageable for long‑term investors as clarity improved.

That pattern reflects what we often see in real time: Markets quickly reprice uncertainty, then return to fundamentals like growth, earnings, policy and liquidity. Even when geopolitical events were unsettling, history shows that many were ultimately manageable for long‑term investors as clarity improved.

A Calm, Planning‑Based Response

Unease is a normal response to uncertainty. The goal of planning is not to ignore risk, but to prepare for how we’ll navigate it. Steps we can help you take right now include:

- Maintaining adequate liquidity so spending needs don’t depend on forced selling

- Using simple, documented rebalancing rules and if-then triggers to avoid emotion-driven decisions

- Aligning portfolio risk with time horizon and goals so that volatility is tolerable

We’re not saying you should ignore the headlines—instead, our message is “let your plan set the course, not fear.”

Your RWA advisory team is monitoring developments and assessing risks to energy supply, inflation and policy. We’re making thoughtful adjustments where we believe they are warranted but not wholesale changes dictated by a single week of news.

We’ll keep you updated as conditions evolve. If you’d like to revisit your plan, spending approach or portfolio considering recent volatility, your RWA team is here to help.

Our Latest Media

In CIO JP Powers’ March Market Update, he gives his perspective on the economic and market outcomes of the ongoing conflict with Iran. He covers how stocks have fared across international markets and U.S. sectors and what’s happening in the bond market. He also reviews private credit as an asset class and puts a spotlight on some encouraging trends in the economy. Watch now.

In the latest episode of The Human Side of Wealth podcast, host Andrew Busa, director of private wealth financial planning, is joined by Senior Advisor and Partner Rick Winters and President of Private Wealth Steve Reder to explain why 2026 could be a pivotal year for proactive tax planning and how the One Big Beautiful Bill Act may impact you. Learn the difference between tax prep and tax planning, why many provisions are “permanent … until changed” and how to use today’s historically low rates to your advantage. Watch now to see how intentional, year-round planning may help you minimize taxes over a lifetime—not just in April.